Berkshire Hathaway's 2024 Proxy Statement

Skin in the game, Repurchase activity, and Stock based compensation

Berkshire Hathaway’s annual meeting is scheduled for Saturday, May 4 at 4:00 p.m. central time. Prior to the annual meeting, Warren Buffett will answer shareholder questions for nearly five hours starting at 9:15 a.m. During the morning Q&A session, Mr. Buffett will be joined by Vice Chairmen Greg Abel and Ajit Jain. During the afternoon session, Mr. Buffett and Mr. Abel will continue to answer questions.

On March 15, Berkshire released its annual proxy statement containing information regarding the formal meeting of shareholders along with a guide for visitors who will attend the shareholder weekend in Omaha. The meeting will be webcast on CNBC and shareholders can submit questions to Becky Quick who will be responsible for selecting half of the questions. Shareholders in attendance can enter a drawing for a chance to ask questions directly.

Berkshire’s proxy is unusually brief and devoid of the usual public relations verbiage that is the norm for most public companies. I have written about Berkshire’s proxy on several occasions in the past, most recently in 2022 and 2023, and several years ago I wrote an article on how to review proxy statements in general.

This article avoids repeating the content from past years and only highlights a few developments that seem worthy of discussion.

Berkshire Hathaway’s 2023 Results

I’ve published a series of articles about Berkshire Hathaway’s 2023 annual report:

Berkshire Hathaway’s 2023 Results — Overview, February 26, 2024

Berkshire Hathaway’s 2023 Results — MSR, February 28, 2024

Progressive vs. GEICO — 2023 Results, March 5, 2024

Burlington Northern Santa Fe — 2023 Results, March 9, 2024

Berkshire Hathaway Energy’s Uncertain Future, March 15, 2024

Skin in the Game

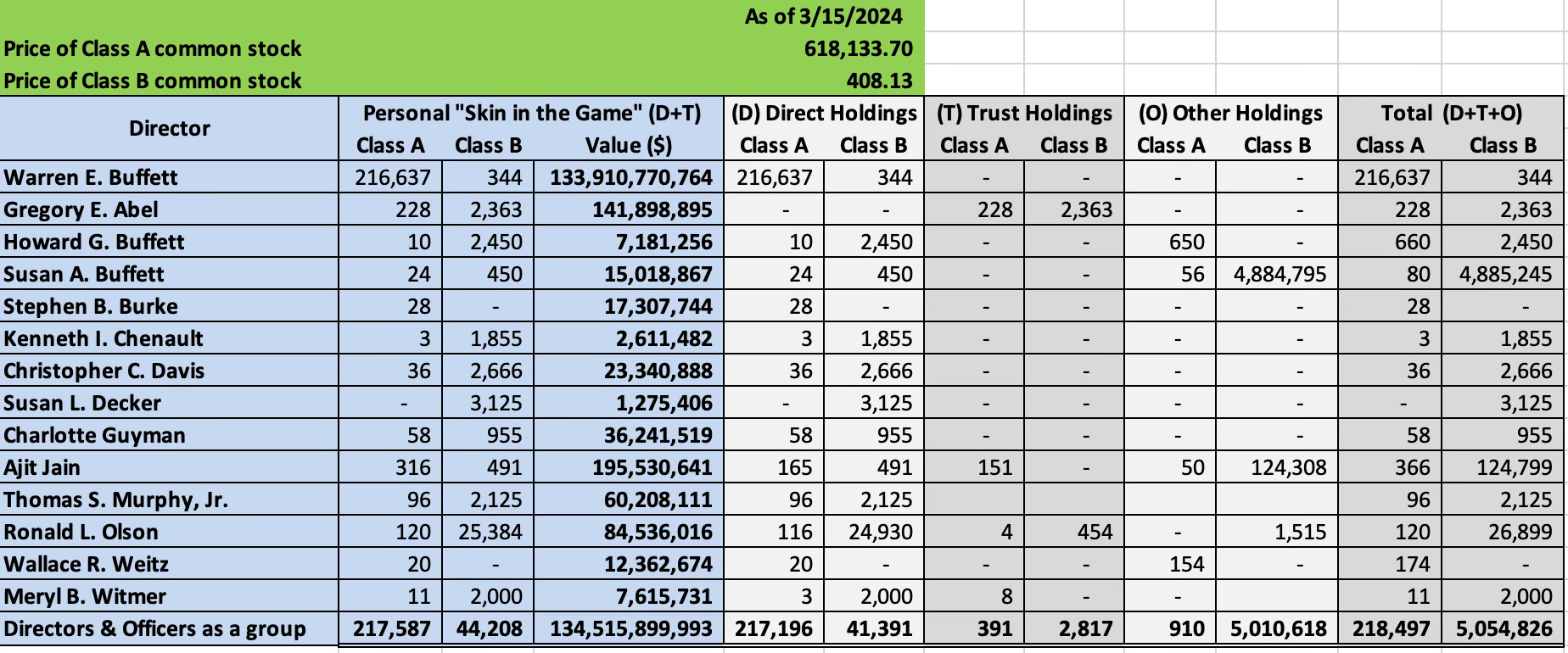

Let’s begin with an updated presentation of the ownership stakes of Berkshire’s Board of Directors. Berkshire Hathaway has long had a policy of requiring directors to have a “significant investment in Berkshire shares relative to their resources.” Unlike most public companies, Berkshire does not grant stock-based compensation to directors. Serving on the board requires an investment by directors using their own money, and they must have built their ownership interest several years before joining the board.

Proxy statements include standardized disclosures about director ownership but the format can be somewhat confusing because it includes shares that directors control for charitable foundations. While the oversight of shares for charity is important, I am much more interested in how much the director and family members have at stake.

In recent few years, I have disaggregated director ownership in a way that I find more useful. Using the table in the proxy and the footnotes, I have attempted to separate direct holdings from holdings for a director’s family members and holdings owned by charitable foundations. In some cases, I have made inferences when the footnotes do not explicitly state the nature of a trust. Unless there is a mention of a charitable trust or foundation, I assume that trusts are held for the benefit of family members.

The following exhibit is my interpretation of the information in the 2024 proxy: 1

As an example of a case that required a judgment call, Greg Abel’s ownership is specified as follows in the footnotes:

“Includes 228 Class A shares and 2,289 Class B shares held by a trust for which Mr. Abel is a trustee but with respect to which he disclaims any beneficial interest and 74 Class B shares are held by Mr. Abel as custodian for members of his family but with respect to which he disclaims any beneficial interest.”

I wrote an article about Greg Abel’s purchase of 168 Class A shares in September 2022 for $68.3 million. This purchase of Class A shares took place shortly after Berkshire Hathaway Energy (BHE) purchased Mr. Abel’s 1% stake in BHE for $870 million. In March 2023, Mr. Abel purchased an additional 55 Class A shares for $24.6 million.

My inference is that such a large purchase was placed in a trust for personal financial planning purposes and ultimately is meant to benefit members of Mr. Abel’s family, although it is possible that the beneficiary of the trust is a charity. In general, I only attribute shares to a charity if the footnotes explicitly mention a charity or a private foundation. Otherwise, I assume that shares held in trust benefit a director’s family.

While there is no doubt that Berkshire’s directors have more skin in the game when compared to the majority of directors of public companies, we should note that the bar set by Warren Buffett is very high. What a “significant investment” relative to a director’s resources means can be debated. Every director has at least a million dollars invested in Berkshire Hathaway. A million dollars is a large sum in absolute terms, but debatable in relative terms at least in a couple of obvious cases.

The death of Charlie Munger last year, as well as the deaths of other long-serving Berkshire directors who were contemporaries of Warren Buffett, has obviously been a big negative for Berkshire Hathaway. The company cannot possibly replace men like Charlie Munger but, all things considered, Berkshire’s board remains far better than average, both in terms of skin in the game and the level of business experience brought to the table. In the decades to come, the owners of the dwindling number of Class A shares will determine board composition and the future of the company.

Repurchase Activity

The proxy indicates that the following shares were outstanding as of March 6, 2024:

Class A: 563,678 shares

Class B: 1,310,995,008 shares

Class A Equivalents: 563,678 + (1,310,955,008/1500) = 1,437,675 sharesThis 10-K indicates that the following shares were outstanding as of February 12, 2024:

Class A: 566,618 shares

Class B: 1,310,805,008 shares

Class A Equivalents: 566,618 + (1,310,805,008/1500) = 1,440,488 sharesFrom this information, we can infer that Warren Buffett repurchased 2,813 Class A Equivalent shares between February 13 and March 8, a span of eighteen trading days. During this period, 253,300 Class A shares traded between $590,340 and $647,039 according to Yahoo! Finance. We will not know the specific price paid for the repurchases until the first quarter 10-Q is released in May, but if we take assume an average price of $612,000 per share, the repurchase cost approximately $1.7 billion.

As of December 31, 2023, there were 1,441,483 Class A Equivalent shares outstanding, implying a repurchase of 3,808 Class A Equivalents between January 1 and March 8. Warren Buffett continued to repurchase shares even as Class A shares broke through $600,000, perhaps validating my sense of the stock being in a “zone of reasonableness” despite its recent spike. Berkshire’s policy is to only repurchase shares if Mr. Buffett believes they are trading below a conservative estimate of intrinsic value.

Stock Based Compensation

I noticed a potentially meaningful change in the language used in the proxy related to stock based compensation.

Here is the language used in the 2023 proxy:

“The Committee has established a policy that neither the profitability of Berkshire nor the market value of its stock are to be considered in the compensation of any executive officer. Under the Committee’s compensation policy, Berkshire does not grant stock options to executive officers.” [Emphasis added]

Here is the language used in the 2024 proxy:

“The Committee has established a policy that neither the profitability of Berkshire nor the market value of its stock are to be considered in the compensation of any executive officer. Under the Committee’s compensation policy, Berkshire never intends to use Berkshire stock in compensating employees.” [Emphasis Added]

While this change might seem subtle, the language in the 2024 proxy seems materially stronger due to the phrase “never intends.” This implies a policy meant to persist long into the future, not merely the present policy of the company.

Berkshire’s avoidance of stock-based compensation, both for executive officers and for directors, has been a defining element of the company’s culture. It appears that this policy is being further enshrined into the fabric of the culture with the intent of persisting long after Warren Buffett leaves the scene. It remains to be seen how executive compensation will be set for future CEOs if “neither the profitability of Berkshire nor the market value of its stock are to be considered” in setting pay.

As Berkshire’s future CEO, Greg Abel has a very large ownership interest in Berkshire Hathaway. Both Greg Abel and Ajit Jain were paid $20 million in base salary in 2023, a level of pay that is generous but not out of line with how executives are compensated at large companies. As long as Warren Buffett remains at Berkshire as Chairman, shareholders are unlikely to question the methodology used to set pay for Berkshire’s top executives, but in the future I suspect that the board will have to define pay policies more clearly whether it involves stock based compensation or not.

Conclusion

Last year, I concluded with the following comments:

It will be a sad day if Berkshire’s proxy consists of a hundred pages of glossy virtue signaling verbiage twenty years from now. At least for now, I am pleased with a proxy that took thirty minutes to read while giving me all the relevant facts rather than one that required an entire weekend to parse through needless verbiage.

Berkshire remains an unconventional company and I see no risk of sliding into hundred page glossy proxy statements full of virtue signaling nonsense as long as Warren Buffett remains in charge. I am hopeful that the culture of the company will remain intact for many decades to come.

If you found this article interesting, please click on the ❤️️ button and consider sharing this issue with your friends and colleagues.

Thanks for reading!

Copyright, Disclosures, and Privacy Information

Nothing in this article constitutes investment advice and all content is subject to the copyright and disclaimer policy of The Rational Walk LLC.

Your privacy is taken very seriously. No email addresses or any other subscriber information is ever sold or provided to third parties. If you choose to unsubscribe at any time, you will no longer receive any further communications of any kind.

The Rational Walk is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com.

Individuals associated with The Rational Walk own shares of Berkshire Hathaway.

In addition to my interpretation of Greg Abel’s ownership interests, I made similar judgment calls regarding the nature of shares held in trust for Howard Buffett, Susan Buffett, Ajit Jain, Ronald Olson, Wallace Weitz, and Meryl Witmer. The footnotes sometimes refer to “charitable foundations” and other times refers to “private foundations.” I interpret “private foundation” to imply a charity. Other references to “trusts” are assumed to be held for the benefit of the director’s family. Obviously, I could be mistaken regarding the ultimate beneficiaries of “trusts” where the nature of the trust is not specified explicitly.

As Warren once said, he plans to manage Berkshire for a while through seances from the grave, the board willing. We can trust that.