Title Insurance

Will the industry's boom turn into a bust in a housing downturn?

Introduction

Property and casualty insurance provides protection against future events. When we buy homeowners insurance, we exchange a relatively small amount of money every year for protection against future property damage and liabilities. Automobile insurance can reimburse us for loss of a vehicle, medical expenses, and liabilities related to a future accident or theft. Most insurance policies will not cover events that took place before a policy was issued. For example, it is not possible to purchase home coverage to pay for damage caused by a hurricane that took place last week.

In contrast to most other forms of insurance, title insurance protects policyholders against past events in exchange for a one-time premium payment. When we purchase real property, it is necessary to ensure that the seller has clear title in the form of a valid and unencumbered deed. A seller who lacks clear title might not be the true owner, or there could be undisclosed liens that impair the seller’s ownership interest.1

Title insurers are responsible for performing an examination of property records to ensure that the seller has proper standing to convey ownership to the buyer. In the event that the title proves to be defective at a later date, the title insurer is responsible for covering losses up to the limit of the policy. For mortgaged properties, the buyer is almost always required by the lender to purchase a title insurance policy that protects the lender up to the mortgage amount. The buyer may optionally purchase a separate owner’s title policy to protect the investment.

In theory, rigorous title examinations should make it possible for title insurers to minimize losses. However, in practice, property records in many parts of the country are not fully digitized and are prone to errors. This is especially true in regions where homes tend to be older and have changed ownership multiple times over many decades. It is far more likely for a single family home dating back a hundred years to have title issues than a condominium in a recently constructed tower.2

For home buyers, title insurance is one of many one-time costs associated with the purchase. The premium for title insurance depends on the price of the property. In 2021, the average premium earned per title insurance policy was slightly over $1,000.3 The low cost of title insurance relative to the cost of the property means that there is an asymmetric trade-off and most buyers do not question the premium.4

Title insurers have major incentives to conduct a thorough title search before issuing a policy and most defects are caught at this stage. If caught prior to the close of the transaction, the seller is responsible for correcting title defects. Only title defects that escape notice prior to the sale can eventually become the responsibility of the insurer.

The economics of the title insurance industry differ significantly from the property/casualty industry. Since the premium is a one-time event that occurs when property changes hands, title insurers do not have the kind of recurring revenue stream that property/casualty insurers have with annual renewals. This makes the industry’s fortunes closely correlated to purchase and refinance activity in the housing market. Losses are relatively rare, but when they occur, the damage can be significant. Title insurers typically have a far lower loss ratio compared to property/casualty insurers, but this is offset by a much higher expense ratio.5

This article provides a high level overview of the title insurance industry with particular focus on the unique economics compared to property/casualty insurance. The industry has been booming over the past few years due to a very strong housing market which naturally led to strong premium growth. Claims are also lower in an environment in which home prices are steadily rising. A slowdown in the housing market due to higher interest rates will likely reduce home purchases and cause refinancing activity to plummet which could cause challenges for title insurers.

Industry Economics

The title insurance industry’s fortunes depend on activity in the real estate market. In the case of an owner’s title policy, coverage remains in force as long as the owner retains title to the property. For a lender’s policy, coverage remains in force until the mortgage is paid off or refinanced. In either case, a premium is collected only once when the policy is issued. Unlike most other forms of insurance, there is no recurring revenue stream for title insurance policies.

The number of policies issued in any period is tightly corrected to home sales and refinancing activity. In periods when interest rates are falling, home sales tend to increase as mortgages become more affordable. When interest rates are rising, home sales tend to decline, and refinancing activity slows down. As a result, the number of policies issued is affected by movements in the prevailing interest rate for mortgages.

The premium that is charged for a title insurance policy depends on the value of the property. It costs more to purchase protection for a more expensive property. As a result, during periods of rising home prices, the average premium paid for title insurance coverage will tend to rise. When home prices are falling, premiums will tend to decline commensurately.

In general, title insurance is highly cyclical, and we can expect premiums to increase during periods of falling interest rates, a rising number of real estate transactions, and rising home prices. When interest rates are rising, the number of real estate transactions are falling, and home prices are declining, premiums can be expected to decline as well.

Industry Structure

When measured on a nationwide basis, the title insurance industry is highly concentrated. The largest title insurance group is Fidelity National Financial which owns Fidelity National, Chicago Title, and Commonwealth Land Title and has a market share of ~32%. First American Title comes it at second place with market share of ~21% and is followed by Old Republic at ~15% and Stewart Title at ~9%.6

Beyond the top four groups, there are a number of smaller title companies, some of which have a large market share in regions of the country. For example, although Investors Title Company has a nationwide market share of ~1%, the company wrote ~23% of premiums in the first quarter of 2022 in its home state of North Carolina.7

As the saying goes, all real estate is local. Even though the large players control a dominant share of the overall market for title insurance, smaller companies that have longstanding local business ties and expertise dealing with property in specific regions can operate profitably. Particularly in locations where the housing stock is older, the importance of rigorous title searches increases. Understanding local nuances can be a competitive advantage when it comes to spotting title defects.

Few buyers actively shop for title insurance. The title insurer is usually selected by realtors, attorneys, or other professionals involved in a transaction. These third-parties value smooth transactions and tend to gravitate toward service providers who they have worked with in the past. As a result, title insurers with deep roots and business connections in a community have an important advantage.

Recent Trends in Real Estate

Over the past two years, the title insurance industry has benefited from strong housing market tailwinds as the average thirty-year mortgage rate hit record lows under 3% and the median existing home price rose significantly, reaching $407,600 in May 2022, representing a 14.8% annual increase.8

The following exhibit shows the median sales price of new and existing homes sold in the United States over the past two decades with data through the first quarter of 2022. We can see that home prices began to increase rapidly soon after the brief recession that marked the beginning of the pandemic.

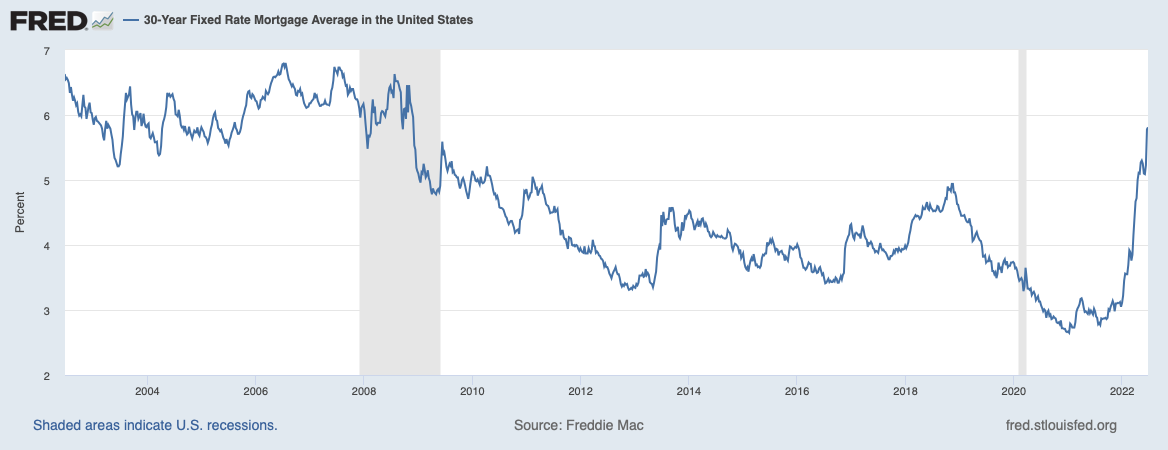

The following exhibit shows the average thirty-year mortgage rate over the past two decades. As the Federal Reserve rapidly cut the Fed Funds rate to near zero and began a large round of quantitative easing in early 2020, mortgage rates plummeted. However, after the average thirty-year mortgage fell to record low levels below 2.75% in 2021, the rate has more than doubled and now stands at 5.81% which is the highest level since before the financial crisis of 2008-09.

As I wrote in March in Trouble Ahead for Housing, housing affordability started to rapidly decline as 2022 began. Since writing that article, the average thirty-year fixed rate mortgage has increased by more than another full percentage point.

Rising home prices and rising interest rates represent a one-two-punch for potential home buyers. Consider this reality from the perspective of an individual closing on a median priced home in June 2021 vs. June 2022 with a 20% down payment and a thirty-year mortgage at the prevailing average interest rate:

June 2021: The buyer puts $71,000 down on a ~$355,000 median priced property and finances $284,000 with a thirty-year mortgage at an interest rate of ~3%. The monthly payment for the mortgage would be $1,197.

June 2022: The buyer puts $81,600 down on a ~$408,000 median priced property and finances $326,400 with a thirty-year mortgage at an interest rate of ~5.75%. The monthly payment for the mortgage would be $1,905.

The need to come up with an additional $10,600 for a down payment and more than $700 per month for a mortgage payment to purchase the median priced home is clearly a huge burden for a typical buyer. Obviously, buyers could attempt to make a smaller down payment, but then the monthly mortgage payment would be even higher and the additional cost of mortgage insurance would be required.

Perhaps unsurprisingly, home sales have been declining recently as mortgage rates and rising prices make homeownership less affordable.9 Existing home sales have declined for four months in a row and transaction activity in May was 8.6% lower than the same month in 2021.10 It seems likely that transaction activity will continue to post year-over-year declines if home prices remain at current levels or increase further and if mortgage interest rates remain elevated.

Over the past two years, the title insurance industry benefited from a housing market buoyed by low interest rates, rising home prices, and a high level of transaction activity. However, with interest rates rising and transaction activity declining, title insurers now face headwinds. The silver lining at the moment is that home prices continue to hit record highs which represents a title insurance market tailwind. However, if home prices plateau or start to decline in response to decreasing affordability, title insurers will face another headwind.

Recent Financial Results

The title insurance industry has been booming along with the housing market. As the following exhibit illustrates, net premiums written have increased from $14.6 billion in 2017 to $26.3 billion in 2021. Most of this growth took place in 2020 and 2021:

This growth has been profitable for the industry as a whole with net income rising every year, most dramatically in 2021. During this period, the combined ratio fell from 100.8% to 94.9%. A combined ratio over 100% indicates an underwriting loss while a combined ratio under 100% indicates an underwriting profit.

What accounts for this increase in profitability?

The industry loss ratio declined from 4.3% in 2017 to 2.3% in 2021. During times of rising home prices, losses decline for several reasons. Title claims tend to rise when the housing market is in distress because various parties have greater incentives to discover title problems under such circumstances. A rising housing market produces the opposite effect. Additionally, every time a home is sold, the old title policy protecting the seller expires extinguishing potential liabilities for title insurers.

The industry expense ratio declined from 96.4% in 2017 to 92.6% in 2021. As we would expect, when premium volume rises quickly, fixed costs should not rise at the same rate. This results in increasing efficiencies which can be expected to bring down the expense ratio.

Trouble Ahead?

The title insurance industry has clearly benefited from a virtuous cycle over the past several years as the housing market boomed due to low interest rates driven by Federal Reserve policies that are now reversing. This has led to the average thirty-year fixed rate mortgage rate more than doubling, but even more trouble could lie ahead.

As the chart presented earlier demonstrates, mortgage rates might seem “high” at the moment, but are still lower than rates that prevailed during the latter stages of the housing bubble. Furthermore, mortgage rates are currently still firmly negative in real terms given the high rate of inflation plaguing the economy.11

Additionally, we can hardly ignore the fact that the Federal Reserve has been a big buyer of mortgage-backed securities in recent years, particularly during the steep run-up of housing prices since 2020, as we can see from the exhibit below:

In May, the Federal Reserve announced its intention to slowly reduce the size of its balance sheet which is informally known as “quantitative tightening”. In June, July, and August, the Fed plans to reduce the size of the mortgage-backed securities component of its balance sheet by $17.5 billion per month. This reduction is supposed to increase to $35 billion per month starting in September.

The reduction of the Fed’s portfolio is supposed to be accomplished by not reinvesting all of the proceeds of maturities and pre-payments, but outright sales of mortgage-backed securities may become necessary as well. Assuming the Fed follows through on its announced plans for “quantitative tightening”, this could be expected to further slow down the housing market.

Conclusion

The title insurance industry has been one of many beneficiaries of a booming housing market over the past two years. The economic fundamentals underpinning the boom appear to be reversing rapidly and it is reasonable to expect a slowdown in the housing market if current trends continue. This will inevitably impact title insurers, particularly those that built up cost structures over the past two years that are difficult to downsize quickly.

Many industries are cyclical but that doesn’t mean they are not worth analyzing and following. Just as market participants often get overenthusiastic about companies in an industry benefiting from tailwinds, unwarranted pessimism can follow during the inevitable downturns. This can present opportunities to those who prepare in advance.

In the aftermath of the housing bubble of the mid-2000s and the financial crisis of 2008-09, market participants punished title insurance companies that were impacted by the cyclical downturn but proved to have successful long-term business models over the past decade. This pattern could repeat again in the coming months and years.

Later this week, I will publish part two of this series which profiles one of the publicly traded companies in the title insurance industry that I have followed for many years.

The Rational Walk is a reader-supported publication

To support my work and to receive all articles that I publish, including premium content, please consider a paid subscription. Thanks for reading!

Copyright, Disclosures, and Privacy Information

Nothing in this newsletter constitutes investment advice and all content is subject to the copyright and disclaimer policy of The Rational Walk LLC.

Your privacy is taken very seriously. No email addresses or any other subscriber information is ever sold or provided to third parties. If you choose to unsubscribe at any time, you will no longer receive any further communications of any kind.

The Rational Walk is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com.

For example, a contractor’s lien can be filed for unpaid debts related to a repair or renovation of the property or a homeowners association can impose a lien for unpaid dues. In more extreme cases, especially for older properties that have changed hands many times, a prior owner or co-owner of the property, or an heir of an estate, could surface and claim that they never signed a deed giving up their ownership interest.

In 2006, I submitted an offer for ten acres of undeveloped land which was accepted by the seller, contingent on a survey. The property line was near the top of a hill and the land descended to a creek. The only buildable site for a house or cabin was near the top of the property adjacent to the road. However, the survey I commissioned showed that the building site was actually located on the adjacent property! I exited the contract. If this had not been caught in the survey, I would have ended up owning unbuildable land with a defective title.

Source: National Association of Insurance Commissioners (NAIC) Report: U.S. Property & Casualty and Title Insurance Industries – 2021 Full Year Results, p. 17.

The principle of loss aversion and regret avoidance comes into play here as well. While a lender’s policy is not optional, a home buyer may decline to purchase an owner’s policy. However, in most cases, regret avoidance would lead a buyer to accept the relatively small cost in exchange for the peace of mind of knowing that he will not lose a major asset in the unlikely event of title problems in the future.

In 2021, the property/casualty industry, in aggregate, had a loss ratio of 72.5% of earned premiums and an expense ratio of 26.3% of premiums adding up to a combined ratio of 99.6%. In contrast, the title insurance industry, in aggregate, had a loss ratio of 2.3% and an expense ratio of 92.6%, adding up to a combined ratio of 94.9%. A combined ratio under 100% indicates underwriting profitability while a combined ratio over 100% indicates an underwriting loss. Source: NAIC U.S. Property & Casualty and Title Insurance Industries - 2021 Full Year Results, p. 1 and 15.

Q1 2022 market share data is provided by the American Land Title Association (ALTA). 2021 market share data is provided by ValuePenguin.com which sources its data from S&P Global. Unfortunately, ALTA’s source data is now provided by subscription only so the link provided above leads to a news release with summary data.

Market share by state can be found at Demotech market share report by Jurisdiction and NAIC Group - Q1 2022. Market share by company can be found at Demotech market share report by NAIC Group and Jurisdiction - Q1 2022.

Data for median home price and existing sales data are taken from the latest National Association of Realtors press release dated June 21, 2022.

While nominal wages have increased over the past year, real average weekly earnings declined by 3% between May 2021 and May 2022. The affordability issue is not a hypothetical question. There have been numerous articles in the media in recent weeks. For example, see What It Takes to Buy Your First Home Now: Interest rates are rising, supply is thin and bidding wars remain widespread. ‘It’s just so ridiculous and disheartening.’ (WSJ)

National Association of Realtors press release dated June 21, 2022.

Inflation was running at a 8.6% annual rate in May 2022.

Excellent piece. Well researched. Easy to understand for the reader.

Q: as the most highly capitalized by value asset class in the US ( by a factor of xxx), a general slowdown would be welcome for the Fed & new buyers.

To what extent does a sticky > 4% through ‘23-24 along w/ an extended slowdown ( recession) play into homeowner psychology insofar as they are having difficulties today w/ lower real wage growth &, persistently high food, energy, oil prices?

Another way to ask is when it’s clear economy is landing hard &, the FED has failed in threading that needle, how much shit do you expect to hit the fan when property markets slows considerably (as stocks - that usually lead the way 1st- by then -year end ‘22 will have lost 30-40% from their Dec ‘21 highs) ?

Thanks. Would be interesting.