Mr. Buffett on the Stock Market

A look back at Warren Buffett's warning about elevated stock valuations in 1999 and the potential application of his ideas to valuations today.

Introduction

In November 1999, Carol Loomis published an article in Fortune based on several informal talks that Warren Buffett had given earlier in the year to groups of his friends. Mr. Buffett made a compelling argument warning investors to curb their enthusiasm for future returns from stocks. I used to read Fortune cover-to-cover and this article had a major impact on my outlook for the future.

A quarter century is nothing in the context of human history, but it is a very long time compared to a human lifespan. Investors old enough to have had meaningful exposure to the stock market of the late 1990s are at least in their fifties today while those who were in senior roles are mostly retired. Young investors now think of the late 1990s in the same way that I thought of the Nifty Fifty bubble of the late 1960s and early 1970s.

Warren Buffett is normally unwilling to discuss the valuation of the stock market or to make predictions but he felt the need to make an exception in 1999.

Why?

He felt that expectations had risen to such a high level that there was virtually no chance that long-term returns could match what people were planning on. I think he felt a duty to warn his friends in private talks and, probably at the urging of Carol Loomis, agreed to publish his concerns for a wider audience.

There is no doubt that expectations were elevated in late 1999:

“Today, staring fixedly back at the road they just traveled, most investors have rosy expectations. A Paine Webber and Gallup Organization survey released in July [1999] shows that the least experienced investors — those who have invested for less than five years — expect annual returns over the next ten years of 22.6%. Even those who have invested for more than 20 years are expecting 12.9%.

Now, I’d like to argue that we can’t come even remotely close to 12.9%, and make my case by examining the key value-determining factors.”

Mr. Buffett goes on to explain his rationale and argue that those who are expecting double digit returns need to justify their assumptions for the underlying factors that he describes. He stressed that he was not predicting what the market would return over short periods like a few months or a year but was looking out over a decade.

More than enough time has passed to conclude that Mr. Buffett was correct about the overall level of the stock market in 1999. Investors who expected double digit returns from the overall stock market were badly disappointed. However, my motivation is not to just confirm that Mr. Buffett was correct in 1999. After I review his rationale for making a bearish long term prediction a quarter century ago, I’ll go on to consider whether a similar warning is justified based on where the same factors stand today.

While I will outline what I view as the essence of Mr. Buffett’s argument, I highly recommend reading his article before proceeding.

Background

To set the stage for his argument, Mr. Buffett begins by observing that the previous thirty-four years could be divided into “an almost Biblical kind of symmetry, in the sense of lean years and fat years.”

From December 31, 1964 to December 31, 1981, the Dow Jones Industrial Average advanced from 874.12 to 875.00. During the same seventeen year period, GDP of the United States rose by 370% while the sales of the Fortune 500 more than sextupled. While investors would have collected dividends during these seventeen years, the price level of the Dow went exactly nowhere.

From December 31, 1981 to December 31, 1998, the Dow Jones Industrial Average advanced from 875.00 to 9181.43. Using a slightly different date range, Mr. Buffett writes that investing $1 million in the Dow on November 16, 1981 would have grown to $19,720,112 by December 31, 1998 assuming reinvestment of dividends. Carol Loomis noted that the Dow had advanced even further to 11,194 by the date of Warren Buffett’s first talk in July 1999.

Obviously, the investor starting out in 1965 had a very different experience in stocks than the equity investor starting out in 1982. This is due to important macroeconomic factors at work during these years that represented a massive headwind in the first period and a strong tailwind in the second. The purpose of Mr. Buffett’s article is to provide an explanation for the radically different performance of stocks during these seventeen year periods, putting into context what seems like a wild situation.

Interest Rates

The level of interest rates has a major influence on the valuation of all investments.

“[Interest rates] act on financial valuations the way gravity acts on matter: The higher the rate, the greater the downward pull. That’s because the rates of return that investors need from any kind of investment are directly tied to the risk-free rate that they can earn on government securities. So if the government rate rises, the prices of all other investments must adjust downward, to a level that brings their expected rates of return into line. Conversely, if government interest rates fall, the move pushes the prices of all other investments upward. The basic proposition is this: What an investor should pay today for a dollar to be received tomorrow can only be determined by first looking at the risk-free interest rate.”

Mr. Buffett goes on to note that the effect of changes in interest rates can sometimes be obscured when it comes to equities because other variables are simultaneously at work as well. But like gravity, the pull of interest rates remains ever-present.

During the seventeen lean years from the end of 1964 to the end of 1981, the interest rate on long-term government bonds moved from just over 4% to more than 15%. This tremendous upward move depressed the value of all investments including stocks. This explains why stocks went nowhere for seventeen long years even as the economy grew substantially over the same period. Stocks had to fall to provide prospective returns competitive with earning 15% on long-term government bonds.

Federal Reserve Chairman Paul Volcker’s aggressive interest rate increases finally ended the inflationary spiral of the late 1970s and early 1980s. This caused interest rates to fall dramatically. Mr. Buffett writes that an investor who put $1 million into the 14% 30-year U.S. Treasury bond issued on November 16, 1981 and reinvested coupons would have ended up with $8,181,219 by the end of 1998 when long-term government bonds yielded around 5%. This compound return of more than 13% was remarkable for a government bond, but stocks did even better compounding at 19%.

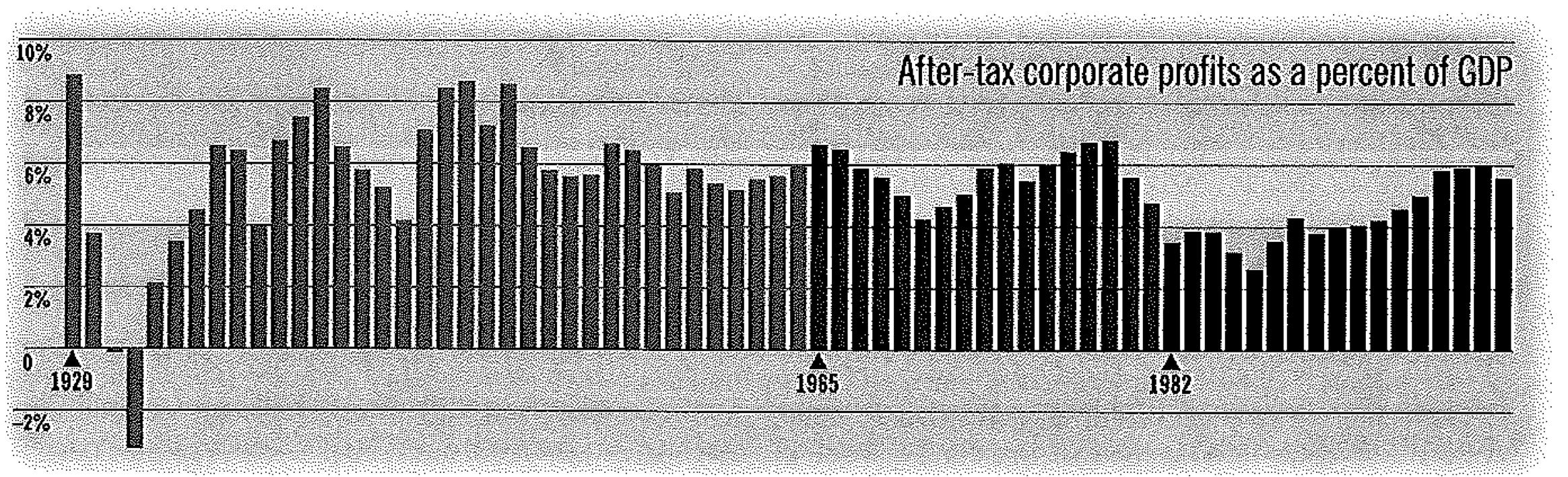

After-Tax Corporate Profits

The profitability of American business is the second factor discussed in the article. Mr. Buffett examined after-tax corporate profits as a percentage of GDP. Starting in 1951, this figure generally remained in the 4% to 6.5% range but by 1981 profits fell to 3.5% of GDP. The fact that corporate profits were depressed at a time of sky-high interest rates were two major factors for the depressed stock market of the early 1980s.

“… As is so typical, investors projected out into the future what they were seeing. That’s their unshakable habit: looking into the rear-view mirror instead of through the windshield. What they were observing, looking backward, mad them very discouraged about the country. They were projecting high interest rates, they were projecting low profits, and they were therefore valuing the Dow at a level that was the same as 17 years earlier, even though GDP had nearly quintupled.”

While GDP did not quite triple from the end of 1981 to the end of 1998, interest rates declined from ~15% to ~5% and, as we see from the chart, after-tax corporate profits recovered back into a more normal range. By the end of 1998, profits were running close to 6% of GDP which was the upper end of the range of “normalcy” at that time. The combination of the large decline of interest rates and solid profitability delivered the large returns to which shareholders had become accustomed by the late 1990s.

Buffett’s Outlook in Late 1999

Market psychology tends to shift slowly at the beginning of a bull market. Investors remained skeptical and risk averse as the bull market began in 1981. After all, the experience of the previous seventeen years had been abysmal and government bonds offered an alternative to stocks. But, over time, the bull market shifted investor psychology as nearly everyone started to make money. As noted in the introduction, by 1999, a survey showed that inexperienced investors were expecting annual returns of 22.9% while even experienced investors expected 12.9%.

Warren Buffett argued that “we can’t come even remotely close to that 12.9%” and he based his claim on an examination of the likely trajectory of interest rates and profits.

Interest Rates. At the time the article appeared, the risk-free rate was ~6%. Mr. Buffett stated that interest rates would have to fall further in order to provide a further tailwind for stocks. He noted that if the risk-free rate were to fall to 3%, that would nearly double the value of common stocks. He seemed skeptical that this would happen and observed that those who think they can predict such a dramatic decline in interest rates would make the most money in bond options.

Corporate Profits. Mr. Buffett thought that it was “wildly optimistic” to believe that after-tax corporate profits would rise much above 6% of GDP and remain at such levels for a sustained period of time. Competition would tend to bring high levels of profitability down and public policy would resist a greater share of the pie going to investors. In his view, there would be political problems if too much of GDP ends up in the hands of investors.

Mr. Buffett thought that it would be reasonable to project nominal GDP growth of 5% with 2% inflation, resulting in real GDP growth of 3%. He stated that if nominal GDP growth is 5% and there is no tailwind from lower interest rates, the aggregate value of equities will not grow much more than 5% plus a small amount from dividends.

“So I come back to my postulation of 5% growth in GDP and remind you that it is a limiting factor in the returns you’re going to get: You can’t expect to forever realize a 12% annual increase — much less 22% — in the valuation of American business if its profitability is growing only at 5%. The inescapable fact is that the value of an asset, whatever its character, cannot over the long term grow faster than its earnings do.”

Mr. Buffett goes on to urge those who disagree with his outlook to not simply disagree but to provide their assumptions regarding interest rates and profitability. In other words, if you believe that stocks will return 12% a year, you’d have to argue that GDP would grow faster than 5%, that a greater percentage of GDP would end up as corporate profits, or that interest rates will fall, or some combination of these factors.

It was also important to consider the valuation of stocks in 1999. On March 15, 1999, the Fortune 500 had a market value of ~$10 trillion which had to be evaluated against the ~$334 billion of profits the group delivered in 1998. In other words, he estimated that the Fortune 500 was trading at around thirty times trailing earnings.

Another way to look at this is to observe that the earnings yield was about 3.3%. Mr. Buffett stated that “the absolute most that owners of a business, in aggregate, can get out of it in the end — between now and Judgment Day — is what that business earns over time.” To expect double digit returns from a group of businesses with such a paltry earnings yield did not make sense. In addition, trading costs were considerable in the late 1990s. Mr. Buffett estimated that investors in Fortune 500 companies paid well over $100 billion a year for advice and for buying and selling securities!

Mr. Buffett summarized his expectation for future stock returns as follows:

“Let me summarize what I’ve been saying about the stock market: I think it’s very hard to come up with a persuasive case that equities over the next 17 years perform anything like — anything like — they’ve performed int he past 17. If I had to pick the most probable return, from appreciation and dividends combined, that investors in aggregate — repeat, aggregate — would earn in a world of constant interest rates, 2% inflation, and those ever hurtful frictional costs, it would be 6%. If you strip out the inflation component from this nominal return (which you would need to do however inflation fluctuates), that’s 4% in real terms. And if 4% is wrong, I believe that the percentage is just as likely to be less than more.” [Emphasis Added]

Those who lived through the late 1990s recall that it was a time of great optimism regarding technology. Mr. Buffett observed that it is tricky to pick out the winners even when technology is rapidly advancing. Both the automobile and airline industries changed the world during the first half of the twentieth century yet this did not result in sure gains for investors. Of the 2,000 car makes that have existed since the dawn of the automobile age, the vast majority went out of business. Aviation was even worse. By 1992, the aggregate profits made since the dawn of aviation for the airline industry was exactly zero.

“The key to investing is not assessing how much an industry is going to affect society, or how much it will grow, but rather determining the competitive advantage of any given company and, above all, the durability of that advantage. The products or services that have wide, sustainable moats around them are the ones that deliver rewards to investors.”

We should keep this in mind today as we are told about the wonders of artificial intelligence and other emerging technologies. They are nearly certain to change the world but not at all certain to enrich the owners of American business, in aggregate.

2000 - 2016

Warren Buffett was not attempting to forecast stock prices in the short run, but the appearance of the article in November 1999 happened to be well timed. Rather than using the Dow Jones Industrial Average, I will look at the S&P 500 instead since it is a broader-based index and is now the most common standard of market performance.

The S&P 500 closed at 1,420.94 on November 22, 1999 when the article was published and closed the year at 1,469.25. On March 24, 2000, the S&P 500 reached an intraday high of 1,552.87. That proved to be the highest level the index would achieve for more than seven years. On October 11, 2007, the S&P 500 hit an intraday high of 1,576.09. It did not reach that level again until April 10, 2013.1

The following chart shows the S&P 500 for the seventeen year period:

As we can see, the S&P 500 experienced a severe bear market for the first three years of this period, following by a bull market that ended in 2007 but only brought the index to a level slightly higher than where it traded at the turn of the century. This was followed by the severe bear market during the financial crisis followed by a bull market that began in early 2009. The bull market technically continued for the duration of the period, although the S&P 500 came very close to a 20% decline in 2011.

The S&P 500 closed at 2,238.83 on December 31, 2016. For the seventeen year period, the annualized return of the S&P 500 was 2.5%. With dividends reinvested over the period, the total annualized return of the S&P 500 was approximately 4.65%.2

The total return for the S&P 500 fell short of Warren Buffett’s baseline 6% expectation, in nominal terms. Although it would go too far to characterize these years as a disaster, particularly given the fact that the financial crisis came around the midway point, there is no doubt that investors who expected double digit returns at the turn of the century would have been bitterly disappointed. Many no doubt threw in the towel during the financial crisis and experienced negative returns from stocks as a result.

Interest Rates in the 21st Century

Let’s take a look at the trajectory of interest rates since the turn of the century. The following exhibit shows the ten year treasury yield since January 2000:

Recall that Warren Buffett wrote that for stocks to have any chance of providing double digit returns starting in 2000, interest rates would have to fall substantially. Over the seventeen year period, interest rates did indeed fall significantly. The ten year yield was 2.45% at the end of 2016, down from around 6.5% at the turn of the century. A 4% decline in the ten year treasury was a massive tailwind for stock prices, yet the S&P 500 still delivered paltry returns over the seventeen year period.

Recall that Mr. Buffett wrote that if interest rates fell to 3%, the value of stocks would roughly double, holding other factors constant. A tailwind doubling the value of stocks over a seventeen year period would deliver over ~4% on an annualized basis. Arguably, the tailwind should have been even greater since rates fell by more than 3%.

By the end of 2016, market psychology had improved after plummeting during the financial crisis, but stock prices arguably did not fully reflect an assumption that low rates would persist in the long run. The Federal Reserve’s zero interest rate policy (ZIRP) and quantitative easing policies were seen as temporary artificial suppressants for rates and stock investors refused to assign valuations that assumed this would continue indefinitely. By early 2018, with the ten year treasury still yielding under 3%, Warren Buffett said that he “would choose equities in a minute” over bonds.

During the early stages of the pandemic in 2020, the ten year treasury yield approached the shocking level of half of one percent! Of course, investors were not willing to project such low yields forever and macroeconomic considerations kept a lid on stock prices. However, it was quite clear at that point that stocks were likely to provide far more generous returns than bonds.

Corporate Profits in the 21st Century

In 1999, Warren Buffett expressed skepticism that after-tax corporate profits as a percentage of GDP could hold much above 6% for any sustained period of time. He turned out to be incorrect on this point, as the chart below shows:

It is remarkable to see how the share of GDP going to profits increased during the 2000s. Aside from the financial crisis, after-tax profits held above 10% for much of the 2010s. At the end of 2016, the figure stood at just above 10%. This has spiked even higher in recent years to remarkably high levels, with tax cuts representing a tailwind. Although social and political pressures have increased, with progressives vocally criticizing corporate profitability, it is notable that the corporate tax cuts that passed in 2017 were permanent while the individual income tax cuts expire in 2025.

Mr. Buffett’s predictions in late 1999 assumed that rates would not fall dramatically and corporate profits as a percentage of GDP would not rise dramatically over the subsequent seventeen years. Although rates declined precipitously and profits soared, this was not enough to provide outsized returns for investors between 2000 and 2016.

Future Returns from Stocks

Rather than continuing the seventeen year period analysis to consider stock returns between 2017 and 2033, it seems more interesting to think about the returns that stocks are likely to provide starting from our vantage point in early 2024. There is nothing particularly magical about seventeen year periods, but I think we can apply Warren Buffett’s approach to today’s environment in an effort to predict whether stocks are likely to provide generous or lackluster returns over the next decade.

As I write this article, the ten year treasury yield is hovering just above 4% and corporate after-tax profits as a percentage of GDP is close to 11%. The S&P 500’s trailing P/E ratio is 26 and the Shiller P/E is over 30, indicating a substantial degree of investor optimism. Individual investors have grown increasingly bullish on the stock market in recent months.3

Suppose that an investor expects the S&P 500 to provide double digit returns over the next decade. With the trailing earnings yield under 4% and the dividend yield around 1.5%, it is clear that double digit returns will require some sort of tailwind.

Many investors believe that this tailwind will be supplied by lower interest rates in the future, although it is hard to argue that a 4% ten year treasury yield is particularly high. Other investors hope for higher profits, but it seems unwise to expect corporate profits as a percentage of GDP to increase from current lofty levels.

I would not presume to state with any certainty what Warren Buffett would say today if he wrote an update to his 1999 article. However, I think that it is fair to say that anyone expecting double digit returns from stocks from today’s levels should specify their assumptions. Of course, many investors are active stock pickers and hope to outperform the market. This is possible, although difficult, in any environment, but those who are investing in index funds probably should temper their enthusiasm.

Conclusion

I have always credited Warren Buffett with keeping me out of trouble in the late 1990s as stock markets inflated. I was young and very inexperienced at the time. Although I was not yet a Berkshire Hathaway shareholder, I followed all of Mr. Buffett’s statements very closely. The Fortune article proved crucial in my decision a few months later to sell my position in levitating shares of Intel in order to invest in the beaten down shares of Berkshire Hathaway.

It is impossible to predict the return of stocks in 2024 or even over a few years, but we can look at current valuations and be fairly sure that double digit returns over the next decade are unlikely for the owner of an index fund tracking the S&P 500. Interest rates would either have to plummet back to the abnormally low levels of the 2010s or corporate profits as a percentage of GDP would have to rise even further.

Younger investors who are decades away from drawing down their portfolios and entering their peak earning years should probably just continue dollar cost averaging into broad based index funds. The situation is more challenging for those who plan to draw down their portfolios in the near term.

With bonds providing paltry returns relative to inflation and stocks unlikely to provide Lollapalooza results, the typical advice to draw down 4% of a portfolio annually might be on the aggressive side. Unfortunately, investors are always going to be prone to extrapolating recent results into the future and could end up in trouble if we are facing a decade, or maybe even seventeen years, of low returns.

Copyright, Disclosures, and Privacy Information

Nothing in this article constitutes investment advice and all content is subject to the copyright and disclaimer policy of The Rational Walk LLC.

Your privacy is taken very seriously. No email addresses or any other subscriber information is ever sold or provided to third parties. If you choose to unsubscribe at any time, you will no longer receive any further communications of any kind.

The Rational Walk is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com.

I obtained price data for the S&P 500 from a combination of Yahoo! Finance and the references in this Wikipedia article.

This figure assuming dividend reinvestment is an estimate based on the data provided by the DQYDJ website which uses the average level of prices during a month to calculate returns rather than the price on a specific date. The underlying data for this website comes from Robert Shiller’s database.

I have not been able to find surveys of long-run expectations but there have been numerous articles and studies recently that reveal general bullishness. For example, a 2023 study revealed that a large majority of investors expected higher short term stock market returns.

Full on excellent piece of work and analysis. Well done.

I like to think I’m mentally prepared for 5% nominal returns for the next 7-10 years since my withdrawal rate is around 2% and I don’t auto adjust upward for inflation. However, even though I think I’m prepared I have a feeling it will be stressful to go through such a long period of low returns while living off the portfolio. I did OK mentally from 1998-2006 (about a 6% CAGR), but I was working, making pretty good money, and I was a net buyer of stocks (mostly Berkshire), so that was not really too stressful as I thought I was picking up bargains.