Different Types of Mistakes

Overpaying for an investment is undesirable but time can heal many wounds

Introduction

There are an infinite number of ways to make investment mistakes and each market cycle reveals new opportunities for speculators to immolate their money. Playing with leverage and derivatives will eventually end in tears for nearly all individual investors and professionals are hardly immune from occasional bouts of speculative fever. The details change but the desire to get rich quickly is perennial.

Of course, it is possible for investors to make serious errors without using any leverage or derivatives. By misjudging a business, one can pay far too much for an investment. However, there is a huge difference between paying too much for a sound business and buying into a speculative “growth” story that implodes.

Overpaying for a business that is certain to exist and earn substantially more a decade from now will dampen results but is not likely to be catastrophic. As the length of time an investment is held increases, the return realized by a shareholder will converge toward growth of intrinsic value. Buying an investment at a bargain price will represent a tailwind. Paying a fancy price will impose a headwind.

Jane’s Story

Let’s revisit the fictional story of Jane, a 45 year old who received an unexpected inheritance of $750,000 in the fall of 2001. I wrote about Jane eleven years ago when I put together an assessment of Berkshire Hathaway’s performance for the ten year period spanning 2002 to 2011. Here was my description of Jane’s financial position at the time she received her windfall:

Jane was 45 years old at the time, had two years of college education, earned the median wage at a very secure job, and owned a median priced home in Omaha, her lifelong hometown. Although Jane’s only debt was a modest mortgage on her home due to be paid off in twenty years, she had no meaningful savings outside of a small emergency fund and no background or experience investing significant sums of money.

Since she was a resident of Omaha, Jane was aware of Berkshire Hathaway despite not having any experience as an investor. In fact, she attended the company’s annual meeting in April 2001 as a guest of a friend who owned a modest number of shares. Although Jane was impressed with Warren Buffett and Charlie Munger, she did not feel comfortable investing the small amount of savings she held for a rainy day.

Jane went on a brief vacation after receiving her inheritance but was determined not to squander the money. She interviewed a few financial advisors but was unimpressed. Then she remembered attending the Berkshire annual meeting.

Impressed by Warren Buffett’s statements at the annual meeting and after reviewing the past few years of shareholder letters, on December 31, 2001 Jane decided to purchase 10 Class A shares for $75,600 each, a total investment of $756,000. Jane’s time frame for holding her shares was indefinite, although she hoped that the funds would appreciate significantly over the next twenty years to provide a source of funds during her retirement which would begin in 2022.

Jane was an intelligent individual and understood what she was buying in terms of the businesses that Warren Buffett described in shareholder letters, but she was not a financial analyst and did nothing to estimate the company’s intrinsic value. She respected the ethos of the company and trusted management. But she did not have a notion of whether she was paying a high or a low price for the stock.

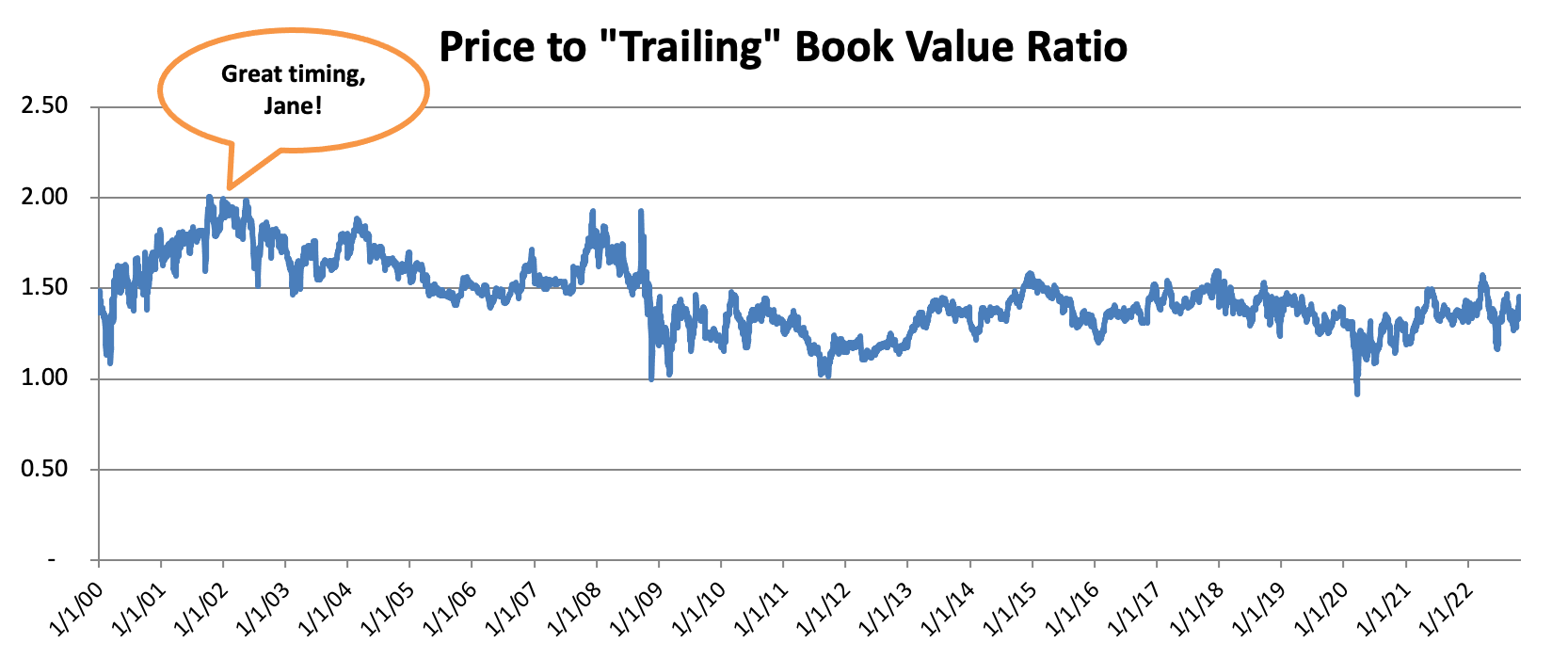

Berkshire’s book value per Class A share was $37,920 on December 31, 2001, so Jane paid very close to two times book value for the stock.

Was this a “high” or a “low” price to pay for Berkshire? In retrospect, we know that Jane paid a very high price relative to book value. Berkshire Hathaway has rarely traded anywhere near twice book value in the years since her purchase.1

Oops … Have fun staying poor, Jane!

Jane managed to pay one of the highest prices for Berkshire relative to book value so far this century! Surely, her results were destined to be dismal after making such a big mistake. Maybe Jane should have hired a financial advisor to avoid this catastrophe?

Not quite.

As I described in my article eleven years ago, Jane ended up doing reasonably well over her first decade of ownership despite paying what was clearly a high price in retrospect.

For the ten year period from December 31, 2001 to December 30, 2011, Berkshire appreciated from $75,600 to $114,755 for a total return of 51.8 percent, or 4.26 percent annualized. Over the same period, a popular exchange traded fund tracking the S&P 500 (SPY) rose from $114.30 to $125.50 while paying $21.88 in dividends representing a total return of 28.9 percent, or 2.57 percent annualized.

No one would call these results spectacular, but it is also not disastrous. Granted, Jane had to hold steady through some gut wrenching declines to achieve this modest return, including a brief trip below her original cost basis during the dark days of March 2009. But Jane was able to hold her shares with confidence because she continued attending annual meetings, reading the annual letters, and generally became more knowledgeable about business and investing concepts.

How did Berkshire do as a business between 2002 and 2011? Until relatively recently, Warren Buffett believed that changes in Berkshire’s book value represented a reasonable proxy for changes in Berkshire’s intrinsic value.2 While Mr. Buffett has long believed that Berkshire’s intrinsic value is far greater than book value, looking at changes in book value between 2002 and 2011 provides some clues regarding how intrinsic value progressed during that decade.

Berkshire’s book value per share was $37,920 on December 31, 2001 and rose to $99,860 as of December 31, 2011. This represents a 163 percent increase, or 10.2 percent on an annualized basis. It is clear that Berkshire’s book value has significantly outperformed the company’s stock price over the ten year holding period of Jane’s investment.

It is reasonable to believe that Berkshire’s intrinsic value increased at an annualized rate of ~10% during Jane’s first decade of ownership. The reason Jane only realized an annualized gain of 4.3% is because the price-to-book ratio that the market assigned to Berkshire declined from 1.99x at the time of her purchase at yearend 2001 to 1.15x on December 31, 2011. Mr. Market loved Berkshire at the end of 2001 and hated Berkshire at the end of 2011. Despite this change in sentiment, Jane’s results were not disastrous because Berkshire’s underlying value increased substantially.

The Rest of Jane’s Story

Jane enjoyed her work and decided to stay employed even though she never earned more than the median income and her Berkshire shares clearly provided the ability to retire early if she chose to. Her continued employment and continued modest spending meant that she never had to sell any of her investment and still owned 10 Class A shares on December 31, 2022 at the age of 65. On that date, Berkshire’s Class A shares last traded at $468,711. Over 21 years, Jane’s investment grew from $756,000 to $4,687,110 representing an annualized gain of close to 9.1%.

We will not know Berkshire’s book value as of December 31, 2022 for a few more weeks. On September 30, 2022, Berkshire’s book value per Class A share was 310,652. From January 1, 2002 to September 30, 2022, book value compounded at almost 10.7%.

Why did Jane’s results fail to fully reflect Berkshire’s business results over her holding period? The reason is that Berkshire’s price-to-book ratio declined from ~2x to ~1.5x. This represented a headwind for Jane. If she had purchased her shares at a price-to-book ratio of ~1.5x, her returns would have matched Berkshire’s growth in underlying business value, to the extent that intrinsic value and book value grew at similar rates.

The important point is that despite paying what proved to be a very high price-to-book multiple for her Berkshire shares, demonstrating truly awful timing, Jane still achieved favorable results over a couple of decades. Berkshire continued to compound intrinsic value at a very satisfactory rate and the initial price paid became less and less important as time went on relative to the importance of business results.

Securely Rich

Jane is in an excellent position to enter retirement due to her wise decision to invest her $750,000 windfall in 2001 rather than consuming it on a more expensive lifestyle. With a paid off mortgage on a home in a relatively low cost city, Jane has few expenses and a $4.7 million investment in Berkshire Hathaway. With Berkshire reliably compounding intrinsic value at around 10% per year in recent years, Jane can safely draw down 3-4% of her holdings every year and face very few risks of ever running out of money even if she eventually faces high long-term care costs or other catastrophes.

By investing in Berkshire Hathaway, Jane has also deferred taxes over a long period of time. She can now convert one of her Class A shares to 1,500 Class B shares and slowly liquidate her holdings during her retirement, benefiting from preferential tax rates on investment income, including the 0% federal tax rate on the first $44,625 of capital gains or qualified dividend income received annually.

It is worth noting that Jane could have invested in the S&P 500 rather than Berkshire Hathaway and achieved reasonably good returns. With dividends reinvested, the S&P 500 would have produced annualized returns of ~8.1% from January 2002 to December 2022. However, taxes would have been due on dividends prior to reinvestment, so Jane’s actual results would have fallen short of 8.1%.

Conclusion

Truly horrific investment mistakes are usually the result of leverage, either applied directly by the investor using margin, or embedded within the capital structure of the companies that are purchased. The recent use of options by individual investors has also led to much pain and misery. Those types of investment mistakes can result in a permanent loss of capital from which there will be no recovery.

In contrast, paying too much for a great business can lead to sub-par results in the long run but will not lead to outright disaster unless the business itself starts to fail. In the short run, paying too much can result in large losses if an investor is forced to sell, but if a great company is held for long enough, it will “grow into” the price that the investor initially paid.

Jane started out as a neophyte investor who just bought into Berkshire because she liked the tone of the annual meeting and trusted Warren Buffett and Charlie Munger. Over time, she gained more knowledge and experience and probably would not have paid so much with the benefit of hindsight. However, she wisely held her shares and just continued to live her life. In time, good business results came to the rescue.

As Jack Bogle might have said, Jane has enough. In fact she has far more than enough and will probably die with a large estate after hopefully living a long retirement. Her “mistake” is a mere footnote in the history of her life. Unfortunately, the same is not true for those who wildly speculate and suffer permanent losses of capital.

Copyright and Disclaimer

Nothing in this newsletter constitutes investment advice and all content is subject to the copyright and disclaimer policy of The Rational Walk LLC.

Your privacy is taken very seriously. No email addresses or any other subscriber information is ever sold or provided to third parties. If you choose to unsubscribe at any time, you will no longer receive any further communications of any kind.

The Rational Walk is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com.

Long Berkshire Hathaway.

The chart plots the daily closing price of Berkshire Hathaway’s Class A shares against the most recent book value, which is why I refer to the chart as price to “trailing” book value.

In his 2018 letter to shareholders, Warren Buffett explained why changes in book value are no longer as meaningful as in the past when it comes to estimating change in intrinsic value.

Outstanding piece. Thank you!

Nice job dude. That was a fun read.