The Risks of Investing in Bonds

Many market observers seem to lack an understanding of the effect of rising interest rates on fixed maturity securities.

Introduction

The social media chatter surrounding the bailout of Silicon Valley Bank and Signature Bank has made it painfully apparent that many market observers lack an elementary understanding of the risks assumed by investors who own fixed maturity securities.

It is not surprising that most people lack a full understanding of the risks, but I have been shocked by many comments on social media made by individuals who should know better. This article might be too basic for many readers, but I have made a point of trying to explain basic personal finance topics in the past and this article is another contribution to that effort.

There are many types of fixed maturity securities of varying complexity. I will not address hybrid securities such as convertibles and I do not address bonds that have inflation protection, such as Treasury Inflation Protected Securities. I have attempted to simplify the discussion as much as possible consistent with conveying basic points.

Types of Risk

At an elementary level, a bond investor provides cash to the bond issuer in exchange for a promise from the issuer to pay interest on a fixed schedule for a certain period of time and to pay back the principal when the bond matures. For example, an investor might agree to pay $1 million for a ten year bond paying 4% interest semiannually. Every six months, the investor can expect to receive $20,000 and at the end of the ten year period, the investor expects the return of his $1 million.

This investor faces the following risks:

Credit Risk. The issuer of the bond might fail to pay the bondholder $20,000 every six months and might not return the $1 million in ten years.

Interest Rate Risk. If the investor needs to sell the bond to another investor prior to maturity, he may not be able to find a buyer who will pay $1 million. If interest rates are higher than 4% when the investor tries to sell the bond, he will have trouble finding a buyer willing to pay $1 million.

Inflation Risk. Even if the bond issuer faithfully pays the bondholder his $20,000 of interest every six months and returns the $1 million in ten years, the purchasing power of those payments might be eroded by high inflation.

Let’s say that the investor is a retiree who is depending on investment income to fund part of his expenses over the next decade. He may not want to take any credit risk whatsoever, even if taking credit risk would result in obtaining a higher interest rate. This is simple to accomplish. The investor can purchase bonds from the United States government and will be assured of receiving timely interest payments and a return of the principal at the end of the ten year period.1

The investor can now sleep well at night knowing that $20,000 is going to land in his bank account every six months for the next decade and that he will receive $1 million of principal when the bond matures. He can “take that to the bank”. The bond is “risk free” in the sense that interest and principal payments will be made on schedule.

Unfortunately, the investor has not eliminated interest rate risk or inflation risk. It is easy to understand why inflation risk has not been eliminated. The bond is going to pay $20,000 every six months for the next decade and $1 million when the bond matures. If prices accelerate faster than expected, that money will not go as far. If the investor is counting on the funds to pay for ordinary expenses of daily life, a high rate of inflation will not be a pleasant experience. This is why you hear people complain about being on a “fixed income” when inflation rears its ugly head.

Understanding interest rate risk is a bit more complicated. If the investor holds the bond to maturity, he will receive par value for the bond, meaning that he will receive the full $1 million back from the government. However, if unexpected events occur over the course of the coming decade and the investor needs his $1 million back early, he cannot simply go to the government and ask for the money to be returned. He will need to find another investor to purchase the bond, and if interest rates are higher than 4%, he will not be able to find an investor willing to pay $1 million.

A Real World Example

Rather than continuing with the scenario described so far, it is more useful to take a real life example since we can observe actual market prices in action.

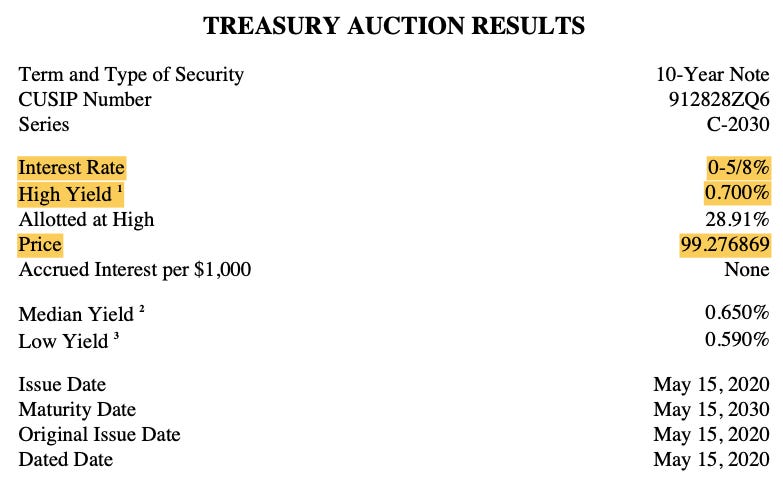

On May 15, 2020, the Treasury announced the results of an auction for a ten year note:

This security represents a commitment by the government to pay a semi-annual coupon of 0.625% for ten years.2 At the end of the ten years, the government will return the principal. When a treasury security is purchased directly from the government, the price is based on a competitive auction. An individual investor who purchased this security via Treasury Direct would have paid a price of 99.276869, the price that was set at auction making the effective yield 0.7%.3

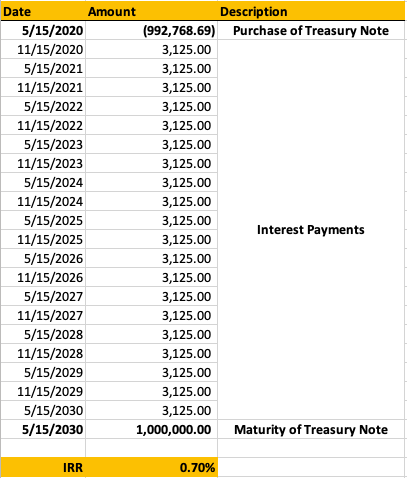

Our investor would have paid $992,768.69 for a bond that promises to pay $3,125 every six months and will receive $1 million when the bond matures. The following exhibit shows the cash flow starting with the initial purchase for the bond on May 15, 2020 and concluding with its maturity on May 15, 2030. As expected, the 0.7% internal rate of return (IRR) for these cash flows corresponds to the yield in the auction result.

It is painfully obvious that this real world example resulted in far less generous payments than would have been the case with a 4% bond. The prevailing interest rate for treasury securities in May 2020 was extremely low. A retiree with a million dollars to invest would receive a pittance in exchange for a ten year commitment. However, there is no doubt that the government would make timely interest payments and the investor is certain to receive $1 million in 2030 when the security matures.

Fast forward to March 15, 2023. Let’s say that our retiree has unexpected expenses and needs to sell the treasury note. At this point, he has received the first five coupon payments. There are still fifteen coupons left before the security matures.

Unfortunately, the retiree cannot just go to Uncle Sam and say, “I’d like my $1 million back today, please.” The government will not redeem the security before maturity. If the investor needs the funds today, he has to find a willing buyer.

Unfortunately, Treasury Direct has no facility to sell securities, so the investor will have to transfer the treasury note to a brokerage firm. Let’s say that he makes the transfer to Fidelity and then tries to sell it to another investor. Here is the screen that the investor will see when he goes to sell the security:

Fortunately, there are investors who are willing to buy the treasury note. Treasury securities are among the most liquid fixed maturity investments in the world and there is always going to be a market if an investor needs to sell. That’s the good news. The bad news is that the bid for this security is 80.455.

I hope our investor is sitting down when he realizes that the treasury note will only bring him $804,550, not his original investment of $992,768.69 and not the face value of the bond of $1 million that he was expecting to receive at maturity.

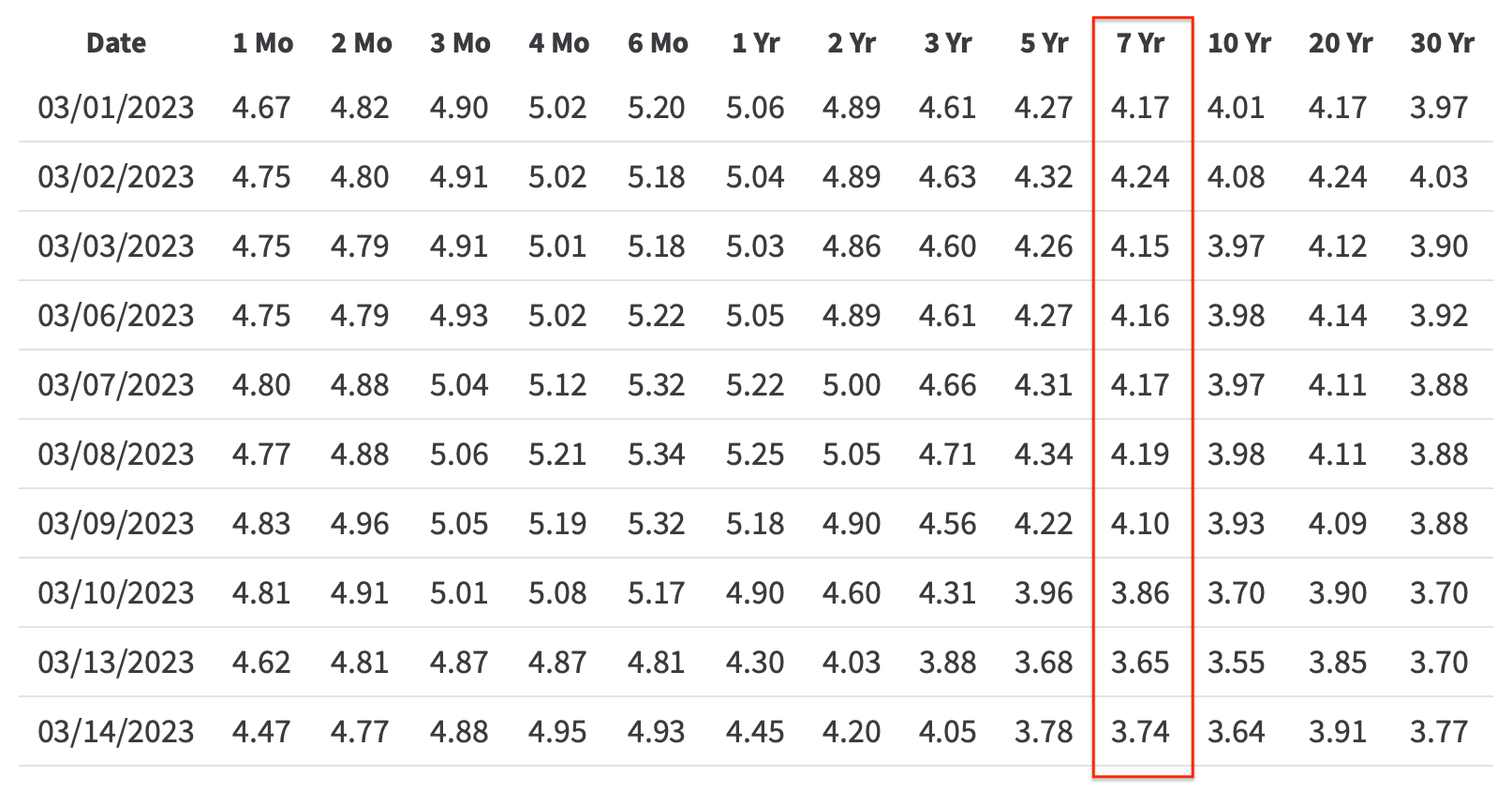

The problem is that interest rates have dramatically increased since May 15, 2020. Let’s take a look at the recent market rates for treasury securities:

Although the original maturity of the treasury note was for ten years, only seven years and two months remain, so we need to look at the current market yield for a seven year note which is around 3 3/4%. That is about the rate a buyer of the bond will demand from our unfortunate investor who must sell the security. In order to achieve a market return, the buyer is only willing to pay $804,550, not $1 million. It is easy to understand why this is the case by looking at the economics of the transaction:

The buyer of the treasury note will benefit from fifteen coupon payments of $3,125 each and will receive $1 million at maturity. The coupon payment remains fixed at 0.625%. In order to earn today’s market rate, the buyer can only pay $804,550 for the security, not $1 million.

If the original investor demands $1 million for this bond, he will not find anyone willing to purchase it because the market interest rate is now around 3.75% for a seven year bond, not 0.625%. There is no reason for any buyer to offer full (par) value for the bond under present conditions.

The bottom line is that the original investor can gain liquidity if he needs it today, but he will take a loss of nearly $200,000!

This loss is incurred because of interest rate risk, not because the government failed to fulfill the promise that was made in May 2020 when the bond was issued.

There is still no credit risk. The government is still willing and able to make the interest payments it promised to the investor and the government will still pay back the $1 million when the security matures. The government is holding up its end of the bargain that the investor agreed to in 2020.

The loss occurs because the original investor cannot find a buyer for his bond who is willing to accept the original terms offered by the government because interest rates are much higher today and it is possible to purchase a brand new treasury note offering much higher interest.

If an investor can buy a brand new seven year treasury note yielding around 3.75%, that is the return you will demand if purchasing a ten year note with around seven years left until maturity.

Conclusion

It is important for investors to understand that there are risks associated with investing in fixed maturity securities. While it is possible to eliminate credit risk by purchasing treasury securities, this does not relieve the investor of interest rate risk.

The degree of interest rate risk that an investor takes is greater for securities that mature in the distant future. If the investor in our example had purchased a three year treasury note instead of a ten year treasury note, it would be maturing soon and he would receive all of his principal back. There would be no need to sell the note to another investor because the government will soon return the principal at par value.

The trouble is that the investor purchased a ten year bond and then needed to sell it after just three years. This required the investor to find another investor to take his place — and in a free market, he could not find someone to pay par value for the security since interest rates have increased substantially. If it is any consolation for the investor, the situation would be far worse if he had purchased a thirty year treasury rather than a ten year treasury.

There is more complexity involved in the bond market than I have outlined in this article, but hopefully the example illustrates the reason for the inverse relationship between bond prices and interest rates and why investors who sell a bond prior to maturity cannot be assured of receiving par value and could suffer substantial losses.

While it is understandable that ordinary people might not be familiar with this topic, it is inexplicable for professional investors, bankers, and financial officers of companies to be ignorant of risks. Loading up on long duration fixed maturity investments carries a great deal of risk, especially when interest rates are low. In a market economy, investors who take such risks must bear the consequences.

If you found this article interesting, please click on the ❤️️ button and consider sharing this issue with your friends and colleagues.

Thanks for reading!

Copyright and Disclaimer

Nothing in this article constitutes investment advice and all content is subject to the copyright and disclaimer policy of The Rational Walk LLC.

Your privacy is taken very seriously. No email addresses or any other subscriber information is ever sold or provided to third parties. If you choose to unsubscribe at any time, you will no longer receive any further communications of any kind.

The Rational Walk is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com.

For purposes of this article, I am ignoring the risk of government default. Despite the drama surrounding the “debt ceiling”, the chance of the government defaulting on treasury securities is extremely remote. If there is a government default of treasury securities, the drama we have seen in recent days will be nothing compared to what will happen.

The semi-annual payment is referred to as a “coupon” because bonds used to be issued in physical form with a coupon that could be redeemed for the interest payment. In today’s world, all of this is done electronically, not on physical paper, but the terminology remains.

The individual investor submits what is called a “non-competitive” bid and receives the high yield that was set in a competitive auction in which larger investors participate.

Nice explanation. The only point I would add is that if our bond investor needs to sell his low interest bond before maturity, he will be taking a loss, but this is not different if he retains the bond. The loss has already been sustained. Selling the bond just means that, for tax and accounting purposes, he is realizing the loss that he had already sustained because of interest rate changes. Likewise, SVB was already insolvent before it started selling its held-to-maturity bonds.

When my children were much younger and I was trying to explain the concepts you just described, I told them that bond buying and selling was a playground for those who love math and can apply math to the real world. Nowadays, all of this is computerized but understanding the concepts, as you demonstrated, is still critical. My more recent message: Don't get involved in games that you don't understand. Thanks for the refresher.