“Good investment ideas are rare, valuable and subject to competitive appropriation just as good product or business acquisition ideas are. Therefore we normally will not talk about our investment ideas.”

— Warren Buffett, Berkshire Hathaway Owner’s Manual

Introduction

The SEC requires institutional money managers holding securities worth $100 million or more at the end of each quarter to file a disclosure report on Form 13F. Although managers are allowed to seek confidential treatment for certain positions, the general rule is that positions must be reported within 45 days of the end of the quarter.

The deadline for reporting positions as of December 31, 2022 resulted in a flurry of filings this week which are available on the SEC’s website. However, it is much easier to use dataroma.com, a website that tracks the activities of 77 super-investors.

There are many serious limitations when it comes to using these reports as a source of investment ideas. Most significantly, 13F reports do not include securities traded on foreign exchanges and short positions are not reported.1 As a result, 13Fs do not necessarily present a complete view of an investor’s portfolio and long positions that are part of long/short pair trades can be misperceived as bullish sentiment on a security. However, the more important limitation is that most managers wait until the end of the 45 day period to report and positions are quite stale as a result. The 13F reports that came out this week show positions that are over six weeks old.

It is tempting to suggest that 13F filings should be more frequent or perhaps even disclosed on a real-time basis. But as Warren Buffett has said, actionable investment ideas are valuable and subject to competitive appropriation. It is natural that investment managers wish to keep their decisions private for as long as possible.

It is a very bad idea to blindly follow a super-investor into a security. There is nothing wrong with considering super-investor portfolios as a source of ideas to look into independently, but this does not appear to be how investors are using 13F filings.

Let’s take a look at two recent high profile examples of coat tailing. The first case worked out badly but the second situation had a considerably happier outcome.

Alibaba

Charlie Munger’s initial investment in Alibaba on behalf of Daily Journal Corporation was revealed in a 13F filing on April 5, 2021. For some reason, Daily Journal files 13Fs very soon after the end of a quarter, so the disclosure reflected the size of the position as of March 31, 2021. The 13F revealed that Daily Journal owned 165,300 shares of Alibaba in the form of American Depository Shares (ADS). Alibaba is a Chinese company but the ADS securities trade on the NYSE so they are included in 13F reports unlike securities traded on foreign exchanges.

The Alibaba position was significant. 165,300 shares at the closing price of $226.73 was worth $37.5 million as of March 31, 2021. This accounted for 12.8% of Daily Journal’s $293.9 million portfolio of marketable securities disclosed on the company’s 10-Q. The data below, provided by dataroma.com, shows how this position evolved over the next two years. Note that dataroma’s figure for % of portfolio shows Alibaba as a 19% position for Q1 2021, not 12.8%. This is because dataroma is only considering securities reported on form 13F as the denominator while my 12.8% figure considers all of Daily Journal’s securities including those traded on foreign exchanges.

Subsequent 13F filings show that Charlie Munger increased Daily Journal’s Alibaba position as the price declined in 2021. He nearly doubled the position during the third quarter and doubled it again during the fourth quarter.

Daily Journal’s Alibaba investment was the lead for the Weekly Digest that I published on March 17, 2022. Here is an excerpt from that article:

Alibaba shares closed at $76.76 on March 15 before rebounding strongly to $104.98 on March 16. If the March 15 low holds, that would represent a 66% decline from the price of the stock when Daily Journal initially disclosed a position at the end of Q1 2021. As the stock price declined last year, Mr. Munger added more shares. Assuming his opinion of Alibaba and China is unchanged from his comments at the Daily Journal meeting, I wouldn’t be surprised if he’s adding even more shares this quarter.

My natural assumption from looking at Daily Journal’s activity in 2021 was that Charlie Munger would probably add to the position, especially since his comments at the 2022 Daily Journal annual meeting still seemed bullish on China. As I mentioned in that article, the situation was interesting to watch from the sidelines but I had no interest in making an investment: “I have always been skeptical about coat-tailing famous investors into situations that I do not fully understand.”

On April 11, 2022, Daily Journal filed a 13F disclosing positions held as of March 31, 2022. Surprisingly, the Alibaba position was cut in half rather than increased. Rather than adding to the position at what many considered to be bargain prices, Charlie Munger reversed course and cut back dramatically.

How would an investor who blindly coat tailed Mr. Munger into Alibaba have fared?

Not well.

Alibaba shares closed at $225.30 on April 5, 2021 when Daily Journal’s position was announced. The closing share price on April 11, 2022 was $101.55, a decline of 54.9%.

At the Daily Journal 2023 annual meeting which took place yesterday, Charlie Munger spoke about the Alibaba investment and characterized it as a mistake. The shares are currently trading at around $104.

Taiwan Semiconductor

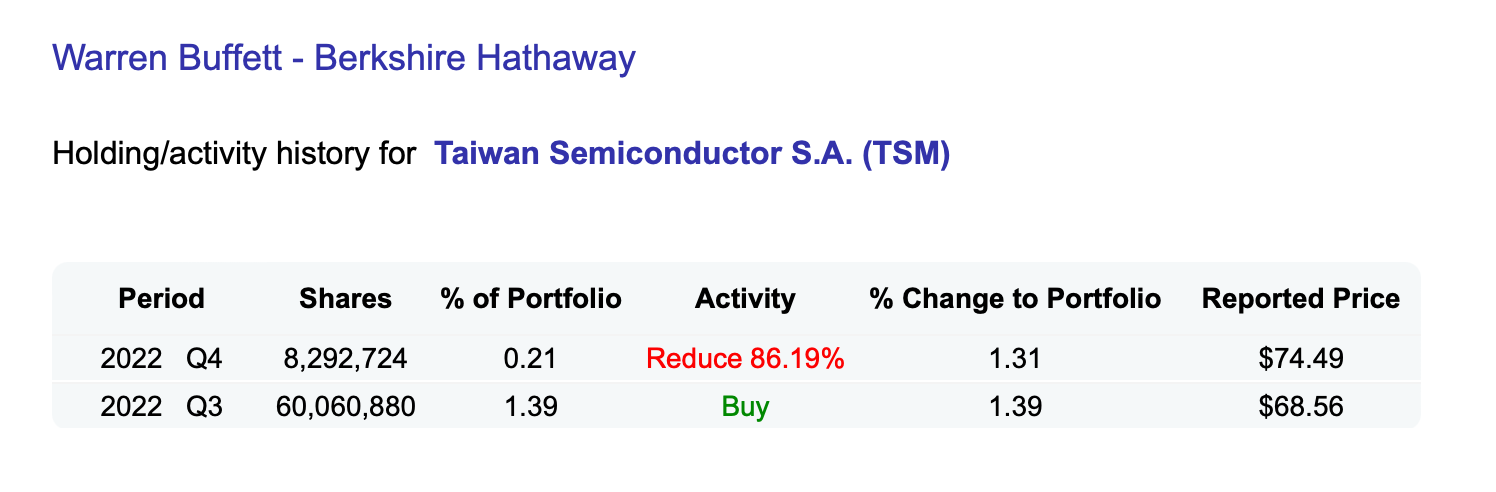

On November 14, 2022, Berkshire Hathaway filed a 13F revealing a large investment in Taiwan Semiconductor American Depository Shares. Berkshire reported owning 60,060,880 shares worth $4.1 billion as of September 30, 2022 based on TSM’s price of $68.56 on that date. The size of the investment led most analysts to believe that the decision was made by Warren Buffett himself rather than one of Berkshire’s other investment managers. This carried a great deal of weight with investors.

The closing price of TSM on November 14, 2022 was $72.80 but the stock opened at $81.92 on November 15 since news of Berkshire’s investment was only known after the market close on November 14. Let’s assume that an investor who coat tailed Warren Buffett into TSM purchased shares at the close on November 15 for $80.46.

It is unusual for Warren Buffett to take short term positions in a company, so most investors were surprised when Berkshire filed its 13F report earlier this week which revealed a drastic 86% cut in the TSM position. This news was revealed on February 14, 2023 after TSM closed at $97.96. On February 15, TSM closed at $92.76.

In our example, a blind coat tailer would have purchased TSM on November 15, 2022 for $80.46 and sold on February 15, 2023 at $92.76 and collected a $0.45 dividend on December 15. This would amount to a total return of 15.8% in just three months, an excellent return in absolute terms as well as relative to the S&P 500. This return was achieved even after accounting for the fact that TSM rallied sharply on the news of Berkshire’s investment in November 2022 and fell on news of the sale this week. The coat tailer would have done well even considering the market’s reaction to the news.

Blind Squirrels Occasionally Find Nuts

One of the examples in this article ended in tears while the other would have worked out quite well. But in both cases, the decision to blindly coat tail a famous investor was not a sound one. Just because a poorly thought out decision works out well does not mean that it was a wise decision. There is a great deal of randomness in financial markets and sometimes factors totally outside of our control deliver good results even when the decision was poor. Of course, the opposite is also true: A well thought out decision can turn out poorly for reasons outside of our control.

The most important reason to avoid blind coat tailing is that an investor can never outsource conviction in an idea. Active investing requires having firm conviction in all decisions. Without conviction, an investor is left totally adrift when the super-investor he is trying to emulate changes course. Most of the time, we have no idea why a super-investor has made a particular decision. But even if we are presented with the entire investment thesis on a silver platter, it would not be our investment thesis because we have not done the work required to have conviction in the conclusions.

True conviction in an investment idea is built up slowly over time through the process of conducting primary research and getting to know a company and its management. To make an idea your own, you must do the work and there are no easy shortcuts. There is no shame in not wanting to do the work. If that is the case, an investor should either entrust funds to a super-investor directly or invest in index funds. Emulating an investor by blinding taking positions revealed in 13Fs is pure folly.

A Useful Starting Point?

I am not against using 13F reports as a source of raw ideas for companies to look into independently. There are thousands of companies to read about and there isn’t anything wrong with knowing what successful investors have owned over time and trying to understand what might have attracted them to the company.

For example, Berkshire Hathaway took a position in Floor & Decor during the third quarter of 2021. When the stock price declined, the position increased dramatically. The size of the investment indicates that it is probably a decision made by one of Berkshire’s investment managers rather than Warren Buffett. But Todd Combs and Ted Weschler are both accomplished investors and also worth following.

Berkshire’s investment in Floor & Decor sparked my interest because I had recent exposure to the company due to a home renovation. In the early summer of 2021, I visited a Floor & Decor location on several occasions to look at different types of flooring. I also visited Home Depot and smaller flooring retailers. Floor & Decor offered the widest array of hard surface flooring in their big box format. Home Depot and small specialty stores only had a small percentage of the variety.2

Although I have not purchased Floor & Decor, it is a company that is now on my radar due to a combination of personal exposure to the business and Berkshire’s investment.

Conclusion

It is tempting to emulate investors who we admire but it simply unwise to blindly follow any other investor into a stock.

When an investor as well-known as Warren Buffett makes a move, the stock typically jumps when a buy is disclosed and falls when there is a sale. We can see this effect with Taiwan Semiconductor. Such moves are driven by investors who are making what are essentially blind bets. Their conviction to hold the stock during difficult times will be built on sand, easily washed away when the first bad news arrives or when the super-investor who bought shares decides to trim the position or exit entirely.

A blind coat tailing strategy will produce both gains and losses on positions due to random factors. But repeated enough times, I suspect that the strategy will produce poor results if the goal is to outperform a passive index over long periods of time.

If you found this article interesting, please click on the ❤️️ button and consider sharing this issue with your friends and colleagues or on social media.

Thanks for reading!

Copyright and Disclaimer

Nothing in this newsletter constitutes investment advice and all content is subject to the copyright and disclaimer policy of The Rational Walk LLC.

Your privacy is taken very seriously. No email addresses or any other subscriber information is ever sold or provided to third parties. If you choose to unsubscribe at any time, you will no longer receive any further communications of any kind.

The Rational Walk is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com.

The SEC proposed short position disclosures in early 2022. I have not been able to locate news about whether these proposals will be adopted.

As an aside, I ended up purchasing carpeting from a small “mom & pop” retailer rather than hard surface flooring. Floor & Decor was the most competitive on price for hard surface flooring, but all of the options were still far more expensive than carpet.

if i respect the investor, i will look at the position but also think independently about it. if i don't respect the investor i don't care what they buy

Many years ago, early 90s, Mr. Buffett commented on investment ideas and people who follow after Berkshire. As I remember it, he wondered why they just didn't buy BRK. He speculated that buying BRK was too easy.