First Republic Bank's Proxy Statement

Large related party transactions reported by the Wall Street Journal were disclosed in the company's 145 page proxy statement, available for all to see for nearly a year.

The Wall Street Journal published an article this morning detailing the compensation of First Republic Bank’s founder along with payments made to his family members in recent years. It is not uncommon for mainstream media articles to report critically about companies that are in the news, as First Republic has been over the past two weeks. Articles of this type are reminders that corporate America is full of cases of excessive compensation and questionable dealings between related parties.

As the article notes, First Republic disclosed matters related to compensation and related party transactions in its latest proxy statement. None of this information should have been remotely surprising to shareholders, regulators, or anyone else who bothers to read proxy statements. I recently wrote about Barney Frank’s compensation as a director of Signature Bank and the research for the article involved reading proxy statements along with other disclosures filed with the regulators.

All investors should read proxy statements, but not all proxies are as brief and to the point as Berkshire’s Hathaway’s proxy which I wrote about last week. There is no excuse not to read Berkshire’s nineteen page proxy which can be accomplished in a half hour. Reading the typical proxy is a lengthier process. While all of the details the Wall Street Journal reported are, in fact, contained within First Republic’s proxy, investors are confronted with a 145 page document replete with ancillary information that is neither necessary nor helpful for an evaluation of management’s performance.

I am not an investor in First Republic and I have not studied the company in detail beyond reading news reports over the past two weeks and taking a look at the balance sheet and related notes. I have also not read every page of the 145 page proxy. However, I thought it would be interesting to briefly go through the proxy to illustrate how salient facts are often buried in a sea of verbiage, much of which is beside the point when it comes to evaluating management. Hopefully, this is helpful for readers who might not be familiar with what to look for in a proxy.

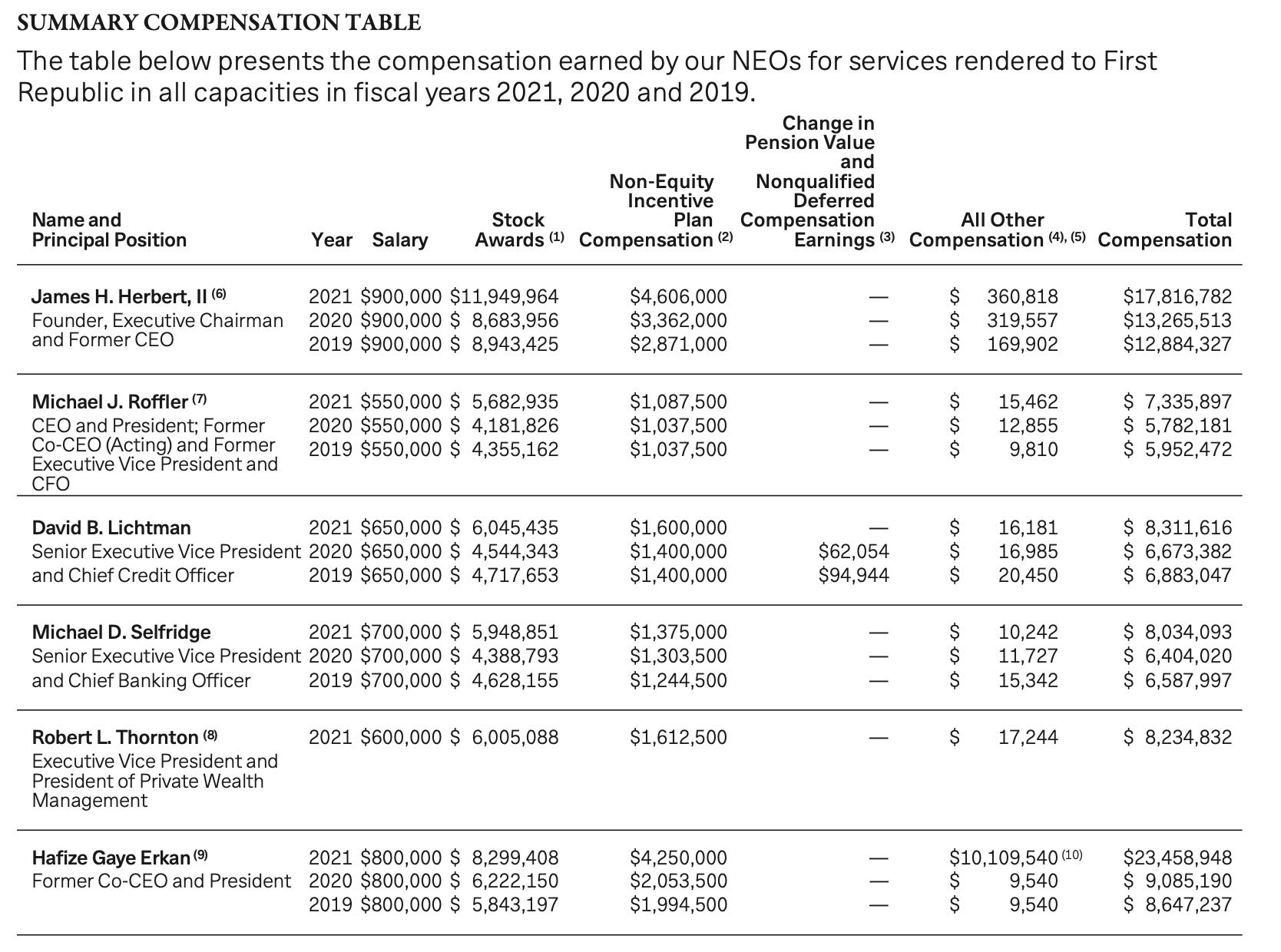

Information about executive compensation appears, in summary form, on page 12 of the proxy and is the source of the Wall Street Journal’s reporting on James H. Herbert’s total compensation of $17.8 million in 2021. In addition to Mr. Herbert, the proxy statement contains information about the total compensation of other executive officers. The table provided by the company appears below:

Former Co-CEO and President Hafize Gaye Erkan’s compensation included $10.1 million of severance following her resignation. Mr. Herbert’s pay is justified on the following page by noting that his total compensation percentile versus a “proxy bank peer group” was at the 79th percentile compared to First Republic Bank’s ranking in the 93rd percentile in terms of growth of tangible book value per share versus the peer group. Interestingly, as disclosed on page 78, the fourteen bank peer group includes Signature Bank and SVB Financial Group, the parent of Silicon Valley Bank.

Several pages follow that detail the company’s diversity policy culminating in a categorization of directors by gender and ethnicity, both of which represent attributes that are irrelevant when it comes to evaluating management competence and performance. Finally, on page 33, we are presented with director pay for 2021:

On page 37, we are presented with a section about “transactions with related persons” which is the source of the Wall Street Journal’s information about financial dealings between the bank and Mr. Herbert’s son and brother-in-law.

James P. Healy, Mr. Herbert’s brother-in-law, is named as the founder and sole owner of a firm named Capra Ibex Advisors. Mr. Healy’s firm advises First Republic “on matters related to the Bank’s investment portfolio, risk management, interest rate and economic outlook and other financial matters pursuant to a consulting agreement effective September 7, 2010, as amended.”

The proxy states that the consulting agreement was negotiated “at arm’s length by Bank management, which did not include Mr. Herbert.” The bank paid Capra Ibex $2.3 million for services rendered in 2021.

Mr. Herbert’s son “is an employee of First Republic primarily engaged in leadership of our Eagle Lending business as a Senior Vice President.” He joined the company in 2017 and earned compensation of $3.5 million in 2021 consisting of “base salary, cash annual incentives and long-term incentives in the form of performance-based RSUs.”

Another related party transaction involves the spouse of David B. Lichtman, EVP and Chief Credit Officer. Mr. Lichtman’s spouse received total compensation of $8.6 million in 2021. Additionally, Mr. Lichtman’s son is a non-executive employee of the bank and received compensation of $323,000. The proxy states that Mr. Lichtman was not involved in setting compensation for his spouse or son. Mr. Lichtman’s spouse has been with First Republic since 1987, predating her marriage to Mr. Lichtman.

One might reasonably ask whether it is plausible that Mr. Herbert’s influence was not a consideration in hiring his brother-in-law’s firm or employing his son. I am sure it is technically true that Mr. Herbert did not set the pay of his son or personally negotiate the terms of the agreement with his brother-in-law’s firm, but it is obvious that Mr. Herbert’s influence would be a factor in the decision making process of whoever was in charge of the financial aspect of those arrangements. After all, Mr. Herbert founded the bank, serves as its Chairman, and is ultimately the boss of whoever actually negotiated compensation with his son and brother-in-law.

These related party disclosures do not, in isolation, prove malfeasance. It is possible that all of the related parties are doing good work for the bank and that they all deserve the payments that have been made. However, the presence of such relationships combined with high pay suggest that shareholders should seek further information from the board. The fact that these relationships are buried in the proxy where few shareholders are likely to read about them does not inspire confidence.

It is interesting to note that the company’s section on “Environmental and Social Responsibility” appears before its section on “Share Ownership”, perhaps unintentionally signaling where the bank places its priorities. On page 51, we are presented with the beneficial ownership of the bank’s executive officers and directors who, in aggregate, control only 0.7% of the shares outstanding, with the majority of that amount controlled by the bank’s founder.

After many pages detailing the company’s very complicated compensation policies, we are presented with the past three years of compensation for the bank’s executive officers which reveals that generous pay has been the norm rather than the exception:

As I mentioned at the beginning of this article, I am not familiar with First Republic Bank or its management beyond reading news reports and spending some time with the financial statements over the past week. I am not interested in potentially owning any of the regional banks that have been pummeled in recent weeks. I have been looking at regional banks out of curiosity and writing about them from the perspective of someone who wants to better understand what has taken place.

With the caveat that I am not an expert when it comes to this bank and am not commenting on the ethics or intentions of its management, it does seem quite obvious that the company has provided generous pay to its executives and directors. It also seems evident that large related party transactions have occurred that should not have been a secret to those who have bothered to read proxy statements.

No investor in First Republic should have been surprised by today’s Wall Street Journal article. All of the information was disclosed in the proxy statement. Proxy statements are unnecessarily long and complicated and part of this might be intentional. It is easy to read a proxy statement that is as brief as Berkshire Hathaway’s but another matter to wade through a sea of verbiage to locate the key passages in a proxy exceeding a hundred pages. But no matter how convoluted a proxy statement might be, it is the responsibility of investors to understand what is in it.

If you found this article interesting, please click on the ❤️️ button and consider sharing this issue with your friends and colleagues. The Rational Walk no longer uses social media. Readers who use social media are encouraged to post links.

Thanks for reading!

Copyright and Disclaimer

Nothing in this article constitutes investment advice and all content is subject to the copyright and disclaimer policy of The Rational Walk LLC.

Your privacy is taken very seriously. No email addresses or any other subscriber information is ever sold or provided to third parties. If you choose to unsubscribe at any time, you will no longer receive any further communications of any kind.

The Rational Walk is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com.

No position in First Republic Bank.

I was asked why I am not interested in buying regional banks despite the carnage. Simple answer is that I delegate this to Buffett. It was widely reported that dozens of private jets landed in Omaha last weekend. No deal so far. If there’s something to do, Buffett will do it. Does that mean others might not want to play in this game themselves? Sure, but I see no reason to think I have any edge playing this game myself. Too much depends on the actions of regulators and politicians. And often fickle depositors in a panic, with people like Ackman spreading panic on social media. Too hard pile for me.

Another excellent article. Thank you. I have invested in 3 banks, all of which Buffett/Munger have current or prior to investment. A lesson learned is that when they divest, I should have followed. The first one was Bank of America, when he bought the preferred with warrants. The dramatic falls of seemingly healthy banks is extremely alarming and reinforces my belief that analysis of such complex financial institutions is best left to Buffett.