Introduction

There are many aspects of life that seem to follow a general pattern: What we know is good for us in the long run seems contrary to what we think is pleasant or pleasurable in the short run.

This is obviously one of the main reasons that people make poor choices regarding food and smoking on a day-to-day basis even though everyone knows, at an intellectual level, that those poor choices will eventually come back to haunt us. Of course, the same issue exists when it comes to personal finances. Almost everyone understands the importance of savings, but our consumer culture bombards us with constant prompts to spend in an elusive quest for immediate gratification.

How is it possible that inflation adjusted per-capita gross domestic product (GDP) in the United States has nearly quadrupled over the past seventy years, yet many people continue to struggle with budgeting to the point where accumulating meaningful savings appears to be an insurmountable task? Take a look at the chart below from the Federal Reserve’s FRED website:

It might be hard to believe, but Americans in the halcyon days of the 1950s were somehow happy living on per-capita incomes in the $16,000 range. To be sure, this is a per-capita number and there were large percentages of the population that were far poorer, particularly minorities suffering from institutionalized discrimination. Nevertheless, the meaning of what it meant to be “middle class” in the 1950s and 1960s would surely be considered to be “poor” in today’s terms.

Consider the typical 70 year old individual who has lived through this remarkable period of economic progress and, assume further, that this hypothetical individual has been right at the per-capita average in terms of personal income. The gains probably appeared to be very gradual over his lifetime, with some bumps along the way. Most likely, he has ratcheted his lifestyle upward slowly over time, perhaps without even realizing it, so the gains never seemed that dramatic. In contrast, let’s say that this individual had an experience similar to Rip Van Winkle and magically fell asleep in 1997 and woke up yesterday. The 30 percent gain in per-capita GDP would likely feel much more noticeable because it was experienced all at once rather than diffused over twenty years. We are conditioned to slow changes in our environment, and these changes blend into the background.

The Virtuous Cycle

Perhaps the most important hurdle to financial independence involves a complete rejection of the ratcheting lifestyle trap and conscious awareness of the enormous abundance of goods and services we enjoy in the United States today compared to previous generations. There is no doubt that disparities continue to exist but, in aggregate, the United States has never been richer than it is today and per-capita incomes have never been higher than today. Why, then, are we made to feel like we are deprived of something if we choose to refrain from continuously ratcheting our lifestyle in lockstep with real GDP?

The virtuous cycle of financial independence is simple to understand: Consumption and savings are two sides of the same coin. What we do not consume can be saved and invested. The less we are accustomed to consuming, the easier it will be to accumulate enough assets to generate passive income sufficient to fund all of our consumption. The flip side is also easy to understand. If we consume nearly all of our income, our savings will be meager in absolute terms and will never accumulate to the point where it is sufficient to generate passive income to meet our much higher consumption requirements.

At the risk of being slightly repetitive, the benefit of a high savings rate is not only the fact that money is accumulating at a faster rate, aided by the power of compound interest. In addition, we make it far easier to reach the day where we reach “escape velocity” and our savings produce passive income sufficient to make working for others truly optional. And there is massive value in having that financial freedom even if one wishes to continue working for others.

The Young Married Couple

It is far, far easier to adopt a Spartan mindset early in life rather than attempting to ratchet back a lifestyle that already consumes the vast majority of your income. The hedonic treadmill concept of psychology makes it clear that we quickly adapt to higher levels of consumption which becomes considered the “baseline”. But the effect is not symmetrical when we cut consumption below that new baseline. To be sure, a rationalization of spending and a reduction to lower levels can be done and has been done by many people, but it is far better to adopt the Spartan lifestyle at an early age.

Let’s assume that we are looking at the situation facing a young married couple who met in college, found meaningful employment after graduation, had two children, and are now 25 years old. They were industrious and frugal for their first couple of years in the workforce and managed to pay off their student debt, which was modest because they attended in-state public universities and also had a little bit of help from family. As a result of this frugality, they retained the “college lifestyle” and are still accustomed to living on a small amount of money every month (around $2,000). The first couple of years in the workforce were successful, they had a couple of children, and they do not plan to have any more.

A good education and industrious habits have resulted in pre-tax income of $100,000 for this two income couple. They are ready to start enjoying more of the fruits of their labor but have had a lifelong goal of achieving financial independence by middle age, not because they necessarily want to “retire”, but because they want to have the option to fully control their time. How realistic is this goal?

Financial Freedom by Age 40

The couple is well positioned to reach their goal due to their $100,000 pre-tax income and the fact that they have diligently kept their monthly spending to around $2,000 per month. Understandably, a couple earning $100,000 would wish to enjoy some of that income as they go through their lives rather than saving everything, but the extent to which they choose to increase spending will have a major impact on achieving their goals.

Let’s assume for the sake of simplicity that the family lives in a state with no income tax such as Texas or Florida. Due to their married status and the benefits associated with having two children, the federal tax burden is relatively modest at around $9,400 using 2016 tax rates (CalcXML’s tax estimator was used to derive this figure). In addition, the couple will owe Social Security and Medicare taxes of $7,650, or 7.65 percent of their gross income. The total income tax burden is about $17,000, leaving the family with $83,000 of after-tax income to allocate.

Let’s say that the couple decides to increase monthly spending by 50 percent to $3,000 per month. That’s a significant increase in monthly spending and should have a noticeable impact on their day-to-day lives. This implies a savings rate of about 55 percent of their $83,000 after-tax income. Actually, that savings rate results in $37,350 available for spending so the family can take a modest vacation in addition to spending $3,000 per month ($36,000/year) on other expenses. They have no savings to speak of today, so they are starting from scratch.

Can this really be done?

From the standpoint of someone earning and consuming $83,000, moving to a 55 percent savings rate will seem agonizing. But it will not be agonizing at all to this family because they are increasing their spending by 50 percent! For them, it is a windfall and will seem luxurious in comparison to their prior lifestyle.

To be sure, spending $3,000 per month isn’t going to result in luxury living but it can go further than many people assume through intelligent and thoughtful spending. However, the upside is that this plan is very likely to result in financial independence for the couple by the time they are 40 years old. Ultimately, it is a matter of priorities. There will no doubt be peer pressure from coworkers and, possibly, family members to consume more given the family’s income. That’s where self control comes into play.

A Look at the Data

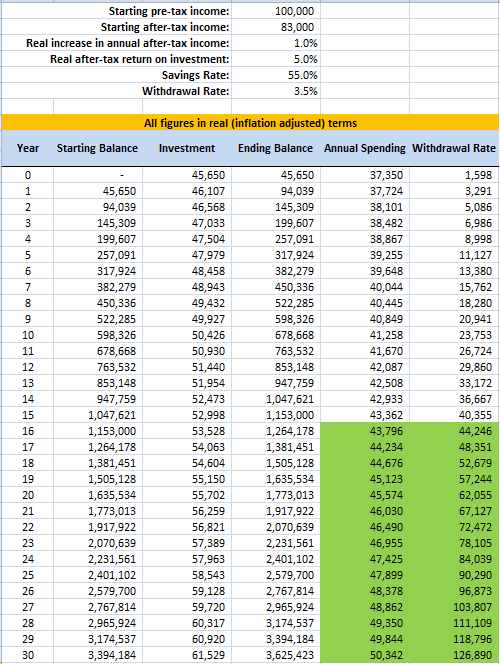

Let’s get down to the specifics of this situation. Here are the assumptions:

The couple earns $100,000 pre-tax and retains $83,000 after tax.

The 55 percent savings rate results in annual spending of $37,350 in the first year.

The family achieves a 1 percent real increase in income annually. In other words, if inflation is 2 percent, the assumption is that the family’s nominal income will rise by 3 percent. The savings rate stays constant over time, meaning that the family increases both real spending and real savings by 1 percent annually.

The real return on investment is assumed to approximate 5 percent. The Standard & Poor’s 500 stock index has generated real returns of approximately 5.4 percent over the past twenty years according to an investment calculator that uses data provided by Robert Shiller.

Assume a withdrawal rate of 3.5 percent of savings. Once the family reaches a savings level where a 3.5 percent withdrawal exceeds annual spending, we consider them to be financially independent.

It is important to emphasize that the figures that appear in the table below are adjusted for inflation and represent real purchasing power using 2017 dollars. Also, note that the family is not totally deprived of increases in their standard of living which we allow to rise by 1 percent annually.

The table shows the starting balance of the family’s savings (which is initially zero), the annual investment assumed to be made in a lump sum at the end of the year, and the ending balance of savings assuming the additional investment along with the 5 percent return. Obviously, in reality, the return will not be a smooth 5 percent but will vary along with the gyrations of the stock market. The final two columns show the family’s annual spending along with the potential withdrawal rate based on the year-end savings balance. The green rows show years when the potential withdrawal exceeds the family’s annual spending – that’s the point at which financial independence has been achieved.

Is it surprising that the family can achieve millionaire status (in real, inflation adjusted dollars) in just fourteen years and be financially independent in fifteen years? Not really, because the power of saving 55 percent of after-tax income coupled with compounding of returns has combined to turbo charge the size of the portfolio. We can see this effect accelerate further after year fifteen, should the family choose to continue working rather than retire. Within 30 years, the family will have savings of over $3.6 million. Even more importantly, that level of savings would allow for annual spending of nearly $127,000, far in excess of what the family is accustomed to.

The Other Path

This is a hypothetical example and the lives of real people including those reading this article will invariably be less perfect and more complex. However, the basic principle remains valid. The path to financial independence involves harnessing the virtuous cycle of limiting consumption and saving an unusually high percentage of income. Doing this will almost inevitably result in financial independence due to the power of compounding over long periods of time.

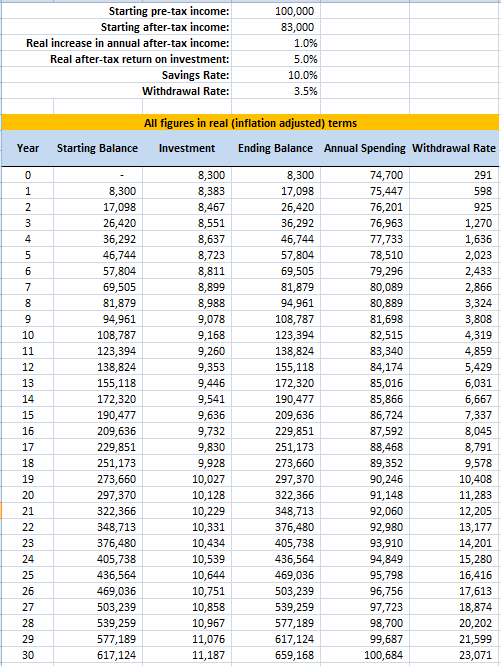

But let’s briefly consider the more typical scenario where the family has taken the advice of financial planning “experts” and saved only 10 percent of after-tax income. Ten percent is considered a “high” rate of savings, and it is compared to the majority of people, but it is totally insufficient to result in savings that will ever replace the family’s much higher level of consumption. Leaving all other assumptions unchanged but changing the savings rate from 55 percent to 10 percent yields the following scenario:

The family is consuming nearly $75,000 per year and saving a paltry $8,300. After 30 years, the savings balance is just over $650,000 which would support annual withdrawals of $23,000, but by that time the family is accustomed to spending over $100,000 per year.

At the age of 55, the couple is not financially independent, and not by a long shot. They can both choose to continue the status quo and work another ten years. At that point, they would finally reach millionaire status with savings of $1.2 million which could generate close to $43,000 in annual withdrawals, but by then they are accustomed to spending over $111,000 per year. So, at the age of 65, the couple will have to make some tough choices. They can cut their consumption and start taking Social Security and should be able to retire. However, cutting consumption will not be any fun, having been accustomed to higher spending for decades, and they will have little margin for error should unexpected expenses come up.

Conclusion

The pursuit of financial freedom is not for everyone. Many people will never do it because they will allow a ratcheting lifestyle to absorb all available resources. Or, as in the “other path” scenario above, they might follow the advice of a “financial expert” and save 10 percent of income and be able to retire by age 65, but not without making compromises after a lifetime of being accustomed to much higher spending. In contrast, thoughtful choices early in life can yield an alternate outcome – financial freedom in early middle age that allows for many additional choices later in life.

Some will inevitably object to the entire premise by claiming that the scenarios completely ignore the utility the couple would get from a higher level of spending over 30 or 40 years compared to the more restrained spending that would allow for early financial freedom. This isn’t entirely invalid since additional spending should lead to increased utility, but beyond a certain level that spending isn’t correlated with a higher level of happiness. Instead, the hedonic treadmill takes over. We become accustomed to the higher level of spending and will notice it when it is gone, but will not get much out of in on an ongoing basis.

Ultimately, the choice is yours to make. And the choice isn’t restricted to a couple that is just starting out either. Someone who is 40 years old could employ the exact same approach to reach financial independence by age 55. The difficulty is that a 40 year old would likely have to adjust spending downward in order to implement the strategy, but “difficult” isn’t synonymous with “impossible”. The tangible and intangible benefits of financial freedom cannot be reasonably attained without making at least a few sacrifices.

Disclaimer: This article is not financial advice. Seek the advice of a financial professional if necessary.