Buffett's Philanthropic Record

Examining seventeen years of Warren Buffett's donations to five foundations

In 2006, Warren Buffett pledged to distribute all of his Berkshire Hathaway stock, representing over 99% of his net worth, to philanthropy. Rather than setting up his own foundation, Mr. Buffett selected five foundations through which he would accomplish his philanthropic goals and wrote letters to each of them regarding the mechanics of how his shares would be distributed.

Mr. Buffett allocated a fixed pool of Berkshire Class B shares for each of the foundations and promised to distribute 5% of the remaining number of shares in the pool on an annual basis.

For example, the initial pool of Berkshire Class B for the Gates Foundation was 500 million shares (adjusted for the 50:1 stock split in 2010). In 2006, the Gates Foundation received 25 million shares, which was 5% of the initial pool. In 2007, the Gates Foundation received 23.75 million shares (5% of the remaining 475 million shares in the pool), and so on. While the number of shares in the pool for the other foundations was lower, the mechanics worked in the same way for all of them.

As Mr. Buffett predicted in his initial letters to the foundations, even though the number of shares distributed would decline by 5% every year, the dollar value of the donated shares could be expected to increase over time since Berkshire’s intrinsic value was likely to grow by more than 5% annually. This has proven to be the case.

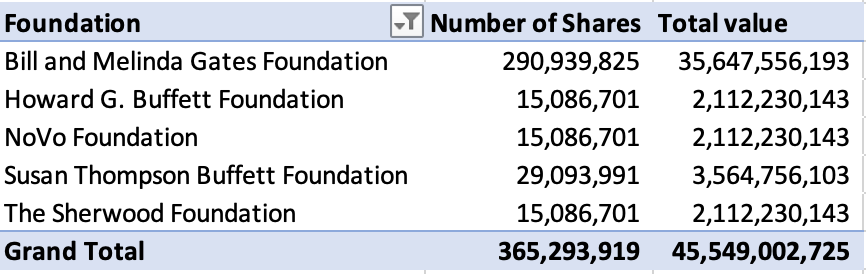

On June 14, Mr. Buffett announced his latest donation of shares to the five foundations. In total, he donated 14,414,136 shares of Berkshire’s Class B stock after converting 9,608 Class A shares into 14,412,000 Class B shares. Berkshire’s Class A stock is convertible into 1,500 shares of Class B stock. Class A shares have 1500x the economic rights of Class B shares and 10000x the voting power of Class B shares.1 The value of the shares donated was $4 billion based on the closing price of $277.64.

In an effort to better understand Mr. Buffett’s philanthropic history, I went to source materials to record the number of shares he donated in each of the past seventeen years.2 The following table shows the total number of shares donated to each foundation along with the market value of the shares based on Berkshire’s Class B share quote on the day of the donation:

In 2021, Mr. Buffett wrote that his ownership in Berkshire Hathaway had halved between 2006 and 2021 as a result of his donations. In June 2006, prior to his first set of donations to the foundations, Mr. Buffett owned 474,998 Class A shares. After the 2021 donations, he owned 238,624 Class A shares. Following yesterday’s donation, Mr. Buffett’s ownership interest is down to 229,016 Class A shares and 276 Class B shares.

Happily for Mr. Buffett and the foundations, the stock has appreciated over the years. Mr. Buffett’s 229,016 Class A shares are currently worth approximately $95 billion. In 2006, his 474,998 Class A shares were worth about $43 billion. Had Mr. Buffett not donated any of his stock, his holdings today would be worth almost $200 billion!

The rest of this article, available to paid subscribers, contains more detailed information regarding Mr. Buffett’s donations over the years as well as a spreadsheet download for those who would like to examine the source data. Additionally, I’ll discuss some of the implications of Mr. Buffett’s conversion of Class A shares to Class B shares prior to making these donations.

Annual Donation History

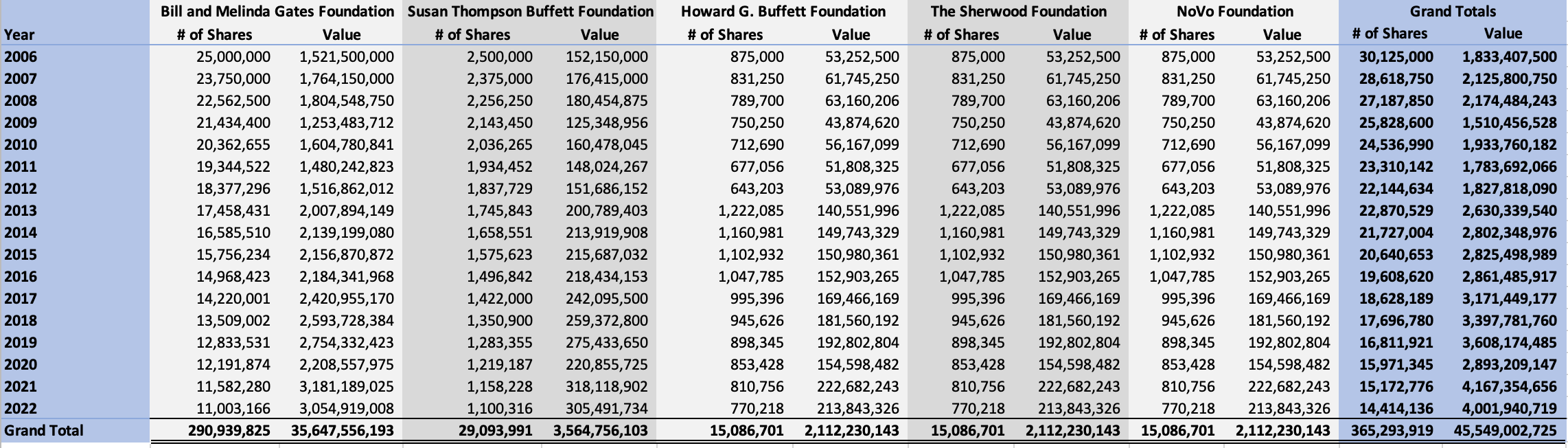

The following exhibit shows the mechanics of Mr. Buffett’s donations to the five foundations. As we can see, the number of shares donated to the Gates Foundation and the Susan Thompson Buffett Foundation have declined over the years. Each year’s donation starting in 2007 amounts to 95% of the shares that were donated in the prior year. In the case of the Howard G. Buffett, Sherwood, and NoVo Foundations, this pattern also holds with the exception of 2013. In 2012, Mr. Buffett decided to double his original pledge for these foundations which are run by his children. This increased the base of shares to be distributed.

Number of Berkshire Class B Shares Donated to Foundations:

Although the number of shares distributed annually has been in constant decline, the value of these shares has increased over time, albeit not in every year. As we can see from the exhibit below, the foundations received substantially more money in recent years than at the outset of the donation program in 2006:

Value of Berkshire Class B Shares Donated to Foundations:

The exhibit below combines these presentations to show the donations each year by total number of Class B shares and market value:

One of Mr. Buffett’s conditions for his donations is that the funds are to be spent by the foundations on their projects in the near term rather than used to expand endowments. Accordingly, it is likely that most of the shares were liquidated to fund charitable operations soon after the donations and something in the neighborhood of the $45 billion in market value was spent.

The shares that were donated would today be worth in excess of $100 billion. It is always interesting to contemplate whether it is better to donate money sooner rather than later. The compounding effect argues for waiting, but there are always needs that are going unmet in the short-run. Mr. Buffett’s approach is something we can all learn from even if the funds we can commit to philanthropy are a microscopic percentage of his immense gifts.

Last year, Mr. Buffett wrote about the trade-off between donating now or allowing compounding to continue over time:

“Had I waited until now to give the shares, they would have instead brought $100 billion to the five foundations. The question then becomes: Would society ultimately have benefitted more if I had waited longer to distribute the shares?

My first wife and I were totally in sync in respect to our philanthropic goals. She, however, favored giving away large sums when we were young – when our net worth was a tiny fraction of its eventual size. I held out for later, remaining charmed by the results of compounding. I was restrained as well by the desire to retain unassailable control of Berkshire. It was only after my wife’s death that I, at 75, stepped on the accelerator.

Deciding when to switch from building philanthropic-destined funds to depleting them involves a complicated calculation based on the nature of the assets involved, family matters, the seldom- confessed instinct to not “let go” and a host of other variables. One size definitely does not fit all.”

A spreadsheet containing the data collected along with links to the source information can be downloaded below.

Implications of Donations

Mr. Buffett’s donations have reduced his economic interest in Berkshire Hathaway, but as I documented in an article earlier this year, his voting interest has not declined very much over time due to the fact that he is converting his Class A shares to Class B prior to making his donations. This has the effect of shrinking the remaining number of Class A shares in circulation and maintaining Mr. Buffett’s ability to control the company even as he has given away more than half of his economic interest.

The following exhibit is taken directly from my previous article and shows that the downward trajectory of Mr. Buffett’s voting control has been very gradual. Recent repurchase activity has actually shrunk the share count faster than Mr. Buffett’s donations have eroded his voting control.

Mr. Buffett will turn 92 years old in August. In 2020, he clarified that all of the shares owned at the time of his death will be distributed to the foundations in the twelve years following his death after being converted from Class A to Class B:

“Looking ahead, Mr. Buffett envisions that all of the Berkshire shares he owns at his death will be distributed to various philanthropic organizations over the following 12 years. Again, “A” shares will be converted to “Bs” immediately before the specified distributions are made. The recipients of the gifts will be obliged to both spend their gifts in a prompt manner and to prevent their use, either directly or indirectly, for any kind of endowment purpose.”

I would expect that the shares will probably be donated in equal installments over the twelve year period which would imply that about 8.3% of Mr. Buffett’s remaining shares would be converted to Class B and distributed annually.

The eventual conversion of Mr. Buffett’s Class A shares raises the question of who will control the dwindling number of Class A shares that will remain in circulation. I wrote the following in March in Berkshire’s Future Depends on Voting Control:

“As the scarcity of Class A shares increases in the future, it is certainly conceivable that the shares will begin to trade at a premium that reflects enhanced voting power. Currently, there is no question that control of Berkshire resides in the hands of Mr. Buffett and the board. However, a couple of decades from now, the configuration of voting control is more uncertain. Those who own Class A shares will have outsized voting power and anyone who wishes to take control of the company or obtain board seats will likely need Class A shares to do so.

As long as Class A shares are not trading for a significant premium above their economic interests in the company (meaning that the price of a Class A share is not significantly more than 1500x the price of a Class B share), it makes sense for anyone who is interested in making a large purchase to opt for Class A shares.”

Long-term owners of Berkshire Hathaway who own more than 1,500 Class B shares might want to consider switching to Class A shares if they can do so in a tax-efficient manner. Each Class A share can be converted to 1,500 Class B shares without triggering a taxable event, but Class B shares are not convertible to Class A. In order to do the swap, one must sell the Class B shares and buy one or more Class A shares in the open market. Doing this in a taxable account only makes sense if there is either a capital loss or a minimal capital gain. But in a tax sheltered account such as an IRA, the switch from Class B to Class A can be done without triggering tax consequences.3

The ESG movement is gaining traction and their proposals might threaten Berkshire’s unique corporate culture. Mr. Buffett’s decision to convert his Class A shares to Class B prior to making donations certainly has made sense during his lifetime since it concentrates voting power in his hands. However, after Mr. Buffett’s death, the remaining charitable donations could have an unpredictable effect on control of the company in the long run.

Copyright, Disclosures, and Privacy Information

Nothing in this newsletter constitutes investment advice and all content is subject to the copyright and disclaimer policy of The Rational Walk LLC.

Your privacy is taken very seriously. No email addresses or any other subscriber information is ever sold or provided to third parties. If you choose to unsubscribe at any time, you will no longer receive any further communications of any kind.

The Rational Walk is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com.

Long Berkshire Hathaway.

For a summary of the differences between the Class A and Class B common stock, read the memo from Warren Buffett dated 2/2/1999 and last updated on 1/20/2010.

The source materials include Berkshire Hathaway press releases, in years when the company issued a press release to document donations, and SEC Filings on Schedule 13 in years when the company did not issue a press release.

This is not tax advice. Consult your tax advisor before taking any actions.

Without the donations, Mr. Buffett would be the wealthiest man today. What he has done to teach capitalism and philanthropy to the masses is unmeasurably valuable. In terms of voting control, I wonder how much Mr. Buffett knows of the large A-share holders, whether they are owned by long-term family / individual shareholders or institutional shareholders. Though unlikely, an opportunistic institution could amass a significant number of A-shares and seek board representation that may weaken the long-term prospects of the company.

The WSJ published a long article today regarding Warren Buffett's gifts to the foundations and speculates about the manner in which his remaining shares will be distributed after his death. Notably, Mr. Buffett stated that there are significant inaccuracies in the reporting, but didn't specify what the inaccuracies are. The WSJ did not address the most important question: Who will control the remaining BRKA shares (and voting control) after the estate is wound down 10 or so years after Mr. Buffett's death.

https://www.wsj.com/articles/warren-buffetts-estate-planning-bill-and-melinda-gates-foundation-sends-charities-scrambling-11655811074?mod=hp_lead_pos10