Berkshire Hathaway: Reinsurance, Inflation, Insider Ownership, and Worst Case Scenarios

This article is the second in a series of responses to questions from readers.

This is the second installment of a three-part series in response to reader questions.

The first article, published on June 21, was about performance disclosures for Berkshire’s investment managers:

Today’s article covers questions about the following topics:

In a few days, I will publish the third and final article covering questions on Berkshire’s retained earnings test and return on invested capital.

To gain full access to all questions and responses, as well as to other exclusive content, please consider a paid subscription. The Rational Walk is a reader supported publication and I appreciate those who choose to support my work.

Thanks for reading!

Reinsurance Outlook

“What is your outlook for Berkshire’s reinsurance businesses? I recall Chris Bloomstran saying that rising interest rates would result in large bond portfolio losses for the competition. Also Ajit mentioned at the Annual Meeting all the cat reinsurance they wrote at the end of Q1 + Warren snapped up Alleghany.”

Business conditions appear to be improving in the reinsurance industry after several years of unsatisfactory results. Toward the end of 2022 and into early 2023, a number of articles appeared about the emergence of a “hard market” in reinsurance. As an example, Insurance Journal published S&P Predicts Reinsurers Will Continue Pricing Momentum During 2023 on January 30 which is worth reading in its entirety.

Reinsurance price increases were “global and broad” according to S&P, necessitated by several years of poor financial returns for reinsurers and a difficult 2022 impacted by losses due to the war in Ukraine, inflation, and catastrophes including Hurricane Ian. Additionally, most reinsurers have a diminished capital position due to mark-to-market losses on fixed maturity investments caused by rising interest rates. Some reinsurers have exited lines of business and imposed new exclusions.

Insurance Journal’s article touches on the role of “alternative capital” which has been an important factor in recent years. With interest rates at microscopic levels for the better part of a decade, alternative capital was attracted to innovations such as insurance-linked securities, a subject that I wrote about several years ago. Now that interest rates are at more attractive levels, the incentive for alternative capital to take risk has been reduced, resulting in reduced exposure to investment vehicles taking catastrophe risk. This adds to the upward pressure on reinsurance pricing.

Berkshire Hathaway has significant advantages starting with the unsurpassed capitalization of its insurance subsidiaries which facilitates the ability of Ajit Jain and Warren Buffett to take on unusually large risks when the price is right.

As I discussed in March in quite a bit of detail, Berkshire’s fixed maturity portfolio is minuscule relative to its equity investments and cash holdings. Berkshire’s fixed maturity portfolio duration is also very short-term which has resulted in minimal mark-to-market losses. I don’t think it is an exaggeration to say that Ajit Jain is in the catbird seat when it comes to taking risks … for the right price.

At the Berkshire Hathaway annual meeting on May 6, Ajit Jain made a number of comments about the reinsurance business during the morning session. I suggest listening to that segment of the video (Question #21).

Here are some of the highlights from my notes:

Property catastrophe has been a difficult business for the past fifteen years. Prices have been unattractive so Berkshire’s presence in property cat has been minimal. In other words, Berkshire just refuses to play when prices are low.

Capacity increased at the end of 2022 which led to Berkshire not deploying as much capital as they hoped to for the December 31 renewal date, an important one in the reinsurance industry. However, the result of that discipline is that they had a lot of “dry powder” for the April 1 renewal date when prices “zoomed up”.

Berkshire is heavily exposed to property catastrophe. Exposure in early May was fifty percent greater than what it was around the start of the year and they have written “as much as our capacity will allow us to write”.

Berkshire has a very “unbalanced portfolio”. If there is a big hurricane in Florida, then Berkshire will face a “very substantial” loss. How substantial? If a major hurricane takes place, Berkshire could lose as much as $15 billion! If not, there will be a profit of “several billion dollars”. (I have been visiting this site frequently.)

Size of exposure is about 5% of $300 billion of capital. This is a level of risk that Ajit Jain and Warren Buffett are willing to accept, obviously at the right price.

Ajit Jain had the following to say about Alleghany:

“In terms of Alleghany, that’s an easy response. We treat our operating units independent of each other. And as far as Alleghany is concerned, they have a major presence in the reinsurance business under the brand name of TransAtlantic Re.

That company will operate the way it’s been operating in the past. There will be no change in terms of strategy or management. And they will keep doing what they’re doing. They’ve been very successful, and hopefully will keep being successful.”

For reporting purposes, Allegheny’s TransAtlantic Reinsurance business has been placed under the Berkshire Hathaway Reinsurance segment, but it appears that decision-making authority for that business will rest with Joe Brandon who has remained CEO of Allegheny under Berkshire’s ownership.

Inflation

“Is there a way to judge how BRK will be able to handle inflation going forward (whether it be low-, middle-, or high-)? Is there a way to estimate pricing power capacity among the wholly-owned companies versus the partially-owned publicly traded companies?”

Warren Buffett mentioned inflation in his 2022 letter to shareholders in a section related to federal taxes:

“Berkshire also offers some modest protection from runaway inflation, but this attribute is far from perfect. Huge and entrenched fiscal deficits have consequences.”

From the context of this comment, Mr. Buffett clearly believes that large fiscal deficits have inflationary consequences. Perhaps he is referring to the massive monetization of government debt implemented by the Federal Reserve since the financial crisis. Whatever the cause might be, Mr. Buffett’s concerns about inflation go back many decades. In 1977, he published How Inflation Swindles the Equity Investor which should be required reading for all investors in today’s environment.

It is difficult to analyze the effect of inflation for Berkshire at the holding company level given that it is comprised of a very large number of businesses with dramatically different economic characteristics. However, we can look at a few examples of businesses that have been impacted by inflation over the past two years:

GEICO has been adversely impacted by higher than expected inflation that caused the cost of repairs and used car prices to skyrocket which directly impacted claims costs. I have written about this several times, most recently in Progressive vs. GEICO: The Battle Continues. On the revenue side, GEICO raised prices and suffered a decline in policies-in-force as a result. In contrast, Progressive has been adding policies-in-force, albeit at the cost of a deteriorating loss ratio that caused management to become more aggressive with rates. In the highly competitive auto insurance industry, inflation seems to be a clear net negative, at least in the short run.

BNSF is an example of a highly capital intensive business requiring frequent large maintenance capital expenditures. During periods of rapid inflation, maintenance capex will accelerate at a faster rate than depreciation based on historical cost. As a result, net income will be overstated and it will be important to examine the railroad’s free cash flow. On a positive note, BNSF does seem to have pricing power. In Q1 2023, operating revenues increased despite much lower physical volumes shipped due to a 14% increase in average revenue per car/unit. I discussed BNSF in more detail in my article on Berkshire’s Q1 results as well as in a much more detailed profile of the railroad published in August 2022.

Berkshire Hathaway Energy is itself a conglomerate partly comprised of highly regulated public utilities which are permitted a certain rate of return on invested capital. Like BNSF, maintenance capex for a capital intensive business like energy will increase at a rate faster than depreciation, but over time this will increase the regulatory capital base and, presumably, revenues should increase with some lag.

Manufacturing, Service, and Retailing is such a broad array of businesses with different economic characteristics that it is hazardous to make any kind of blanket statement. At a very high level, perhaps looking at pre-tax margins can provide a hint of how resilient these businesses are in terms of passing through inflationary costs. In my first quarter article, I included a section on the MSR group which contained a table showing margins on a quarterly basis over the past three years. Overall, margins seem to be holding up reasonably well.

A full analysis of the effect of inflation on each of Berkshire’s subsidiaries (and partially owned stakes in public companies) would be a large project and is beyond the scope of this article. My general sense has always been along the lines of what Warren Buffett wrote in the annual letter. The overall company has some inflation protection but inflation is not a net-positive for Berkshire. I think that Berkshire should handle inflation at least as well as the average large company.

Insider Ownership

“You've previously written about Berkshire's culture and the potential for its endurance when the top leadership eventually changes. I just read in the WSJ that only 0.03% of Disney stock was owned by insiders at the end of Q1, compared to an average of 2.09% for the broader S&P 500. Both including and excluding WEB & CTM, what percentage of BRK stock was owned by insiders at the end of Q1? How meaningful a metric do you think this is for shareholders to watch as the next chapter of BRK unfolds? How important is Greg Abel's personal ownership (is this a dollar amount or % threshold we should watch for)? Is this broader metric (broad insider ownership) more meaningful than obsessing over how many shares Greg Abel personally owns?”

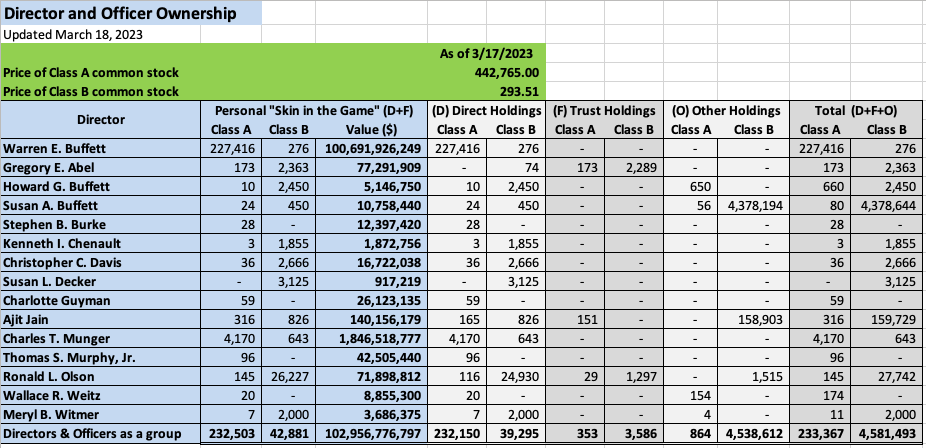

There have been changes since I wrote an article analyzing Berkshire’s 2023 proxy but the overall picture is not much different than the exhibit I made for that article:

There have been two notable developments not reflected in the above exhibit:

Greg Abel purchased an additional 55 shares of Class A stock on March 17 and now holds a total of 228 Class A shares worth approximately $116 million. I wrote an article about Mr. Abel’s initial purchase of Berkshire shares in October 2022.

Warren Buffett made annual gifts to five foundations on June 21. He converted 9,129 Class A shares into 13,693,500 Class B shares before giving away 13,693,432 shares. He currently owns 218,287 Class A shares and 344 Class B shares. (As an aside, I wrote an analysis of Mr. Buffett’s philanthropy last year. It’s an amazing story.)

Last year, I wrote a lengthy article making the case that Berkshire’s future depends on voting control and I followed up with another article proposing a split of the Class A shares to allow long term oriented individual investors to retain their full vote rather than resort to converting to Class B with diminished voting rights in order to gain liquidity while minimizing capital gains taxes.

One of the questions I submitted for the 2023 annual meeting was about what voting control at Berkshire would look like in 2050. Unfortunately, that question was not selected but I think the topic is of utmost importance. At the time, Mr. Buffett controlled 15.6% of the economic interest in Berkshire but exerted 31.6% of the voting control. This figure diminishes somewhat every year due to Mr. Buffett’s gifts, but is ameliorated by the fact that he’s converting his Class A shares to Class B before making the gifts. Even without fifty percent of the vote, Mr. Buffett will almost certainly always get his way during his lifetime.

I don’t want to repeat too much of what I wrote in previous articles other than to say that I have no clear picture of who exactly will own the majority of Berkshire’s Class A stock a decade after Mr. Buffett’s death. At that point, Berkshire’s board will not have more than a small percentage of voting control. If the remainder of the Class A shares are with large institutions and the “ESG” movement is still in vogue, there is no telling how many changes to Berkshire’s culture and management practices will be imposed by people who have voting control but no personal skin in the game.

Of course, voting control is only one aspect of insider ownership. Alignment of incentives is the other important factor to consider. Will having over $100 million in Berkshire stock provide a good enough incentive for Greg Abel to do his best to increase the value of the company in the long run?

From what I know of Mr. Abel, I think that he is going to be highly motivated to do all in his power to maintain Berkshire’s culture over the long run. His stake in Berkshire is not a majority of his net worth but it might be in the future. But he is already an ultra-rich individual and is likely to be just as motivated to do a job that would make Warren Buffett proud of his choice of successor!

To sum it up, my concern is much more related to whether large institutions will gain control of Berkshire in the future and make it impossible for Greg Abel and his successors to run the company in the way that has generated so much value for shareholders under Warren Buffett’s stewardship. I am much less worried about incentives for Greg Abel and other top managers at Berkshire, all of whom are independently wealthy and have significant non-economic motives to do their best.

Worst Case Scenarios

“I'm quite interested in your view about what's the worst potential scenario that could happen to Berkshire, except the nuclear threat Buffett only talked about during the annual meeting.”

If the question did not exclude nuclear war, I would probably write a few paragraphs about that risk, although nuclear war is a “game over” risk for all businesses, not just Berkshire. Forget about business, it is a civilization ending risk. I’m in alignment with Charlie Munger’s sentiments on nuclear war from the 2022 annual meeting: “In the event of a nuclear attack, I’m going to crawl under the table and kiss my ass goodbye.”

I think that it is most productive to consider worst case scenarios for Berkshire that could result in outcomes that are more negative than for the average large publicly traded American business.

While it is tempting to discuss a degradation of culture brought about by voting control passing to “ESG” advocates, I’ve already beaten that risk to death in the above section as well as prior articles. Furthermore, if Berkshire is overtaken by “ESG”, that is not likely to create worse outcomes than for a typical American business. Berkshire will just slide down toward the average. There is no reason to suppose that “ESG” implemented at Berkshire would be worse than how it is implemented everywhere else.

So, what is the most significant risk?

Berkshire is unique in that many shareholders have an unusually large allocation to the company. This is certainly true in my case. Shareholders with a large investment in Berkshire are often there because of Warren Buffett, but that has always seemed like an “added bonus” to me. After all, when I purchased my first shares in Berkshire, Mr. Buffett was already 69 years old. I never dreamt that he would be running the company for another 23+ years.

My large allocation to Berkshire is due to my judgment that this single stock actually represents a very large and well diversified group of businesses.

During the last several years of my time as a W2 employee, I used Berkshire like many investors use index funds. I just kept buying more Class B shares as I had money to save and invest. The fact that Berkshire is a single stock and not an index did not bother me then and does not bother me very much even now. In fact, the company is far more diversified today than it was twenty years ago.

The potential issue in the back of my mind is that Berkshire’s diversified businesses are held in different ways within the holding company, sometimes in ways that are somewhat surprising. For example, BNSF is actually held within National Indemnity rather than directly by the holding company.

The chain of ownership of Berkshire subsidiaries sometimes gives me pause because I do not have a precise understanding of how a problem at one subsidiary might cause contagion in another, or to put in another way, can creditors of an insolvent subsidiary lay claim to assets elsewhere in Berkshire in ways that I might not anticipate?

In the case of BNSF being owned by National Indemnity, the situation is clear. If National Indemnity runs into some horrendous problem, the assets of BNSF are potentially on the hook to meet policyholder and/or creditor claims.

But “contagion” could act in the reverse direction as well. For example, PacifiCorp is facing a potentially large legal liability related to a series wildfires in Oregon in September 2020. Although I doubt that the ultimate damage will reach the $1.6 billion cited in some news stories, this is still likely to be a large liability.

PacifiCorp had shareholders’ equity of $10.3 billion as of March 31, 2023, a significant chunk of BHE’s $47.9 billion of shareholders’ equity. Although the current lawsuit is far less than PacifiCorp’s equity, what if a future catastrophe results in legal obligations bankrupting PacifiCorp? Are there legal or reputational reasons that would cause BHE to bail out PacifiCorp with a cash infusion? Would Berkshire, at the holding company level, have reputational reasons to get involved?

If an investor owns a highly diversified index fund like the S&P 500, there is no real possibility of “legal contagion” between the five hundred companies that are owned. However, that is not necessarily the case when owning an “index” of companies within a conglomerate like Berkshire, so this is a risk worth considering.

I intend to investigate this subject in more depth in the future and if I come up with anything worth writing about, I will share my findings with subscribers.

If you found this article interesting, please click on the ❤️️ button and consider sharing it with your friends and colleagues or on social media.

Copyright, Disclosures, and Privacy Information

Nothing in this article constitutes investment advice and all content is subject to the copyright and disclaimer policy of The Rational Walk LLC.

Your privacy is taken very seriously. No email addresses or any other subscriber information is ever sold or provided to third parties. If you choose to unsubscribe at any time, you will no longer receive any further communications of any kind.

The Rational Walk is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com.

Long Berkshire Hathaway.

Thanks for the valuable information. Really appreciate it.