Barney Frank's Signature Bank Compensation

Apologists for crony capitalism are telling the American people that shareholders and executives of failed banks will be wiped out. The reality is more complex.

Despite the disingenuous and hypocritical statements of billionaire apologists of crony capitalism, the government’s actions last night certainly represent a bailout for the wealthy individuals and corporations that had uninsured deposits at Silicon Valley Bank and Signature Bank. To suggest otherwise is to engage in shameless gaslighting.

I described the bailout earlier today after outlining the problems at Silicon Valley Bank on Saturday and making a plea for the government to resist calls for bailouts on Sunday. Today, we are being told that the system had to be protected “for the good of the economy” but, rest assured, the shareholders, directors, and executives of these failed institutions will suffer severe financial consequences.

I have no doubt that ordinary shareholders of these banks will be wiped out, but don’t cry too much worrying about executives and directors. These highly paid individuals will be just fine and, since there seems to be little shame left in corporate America, most of the bank executives who need to work in the future will find gainful employment. It’s just a short drive up Interstate 280 to Sand Hill Road (Exit 24).

One of the most outrageous aspects of corporate America in the twenty-first century is the extent to which “public servants” in oversight roles are blatantly rewarded with cushy sinecures once they retire. As I read some of the early mainstream media articles on Signature Bank over the weekend, I was bemused to see no references to Barney Frank who has been a director for nearly eight years. Surely the presence of a co-author of the Dodd-Frank Wall Street Reform and Consumer Protection Act on the board of a failed bank that catered to the cryptocurrency industry is big news.

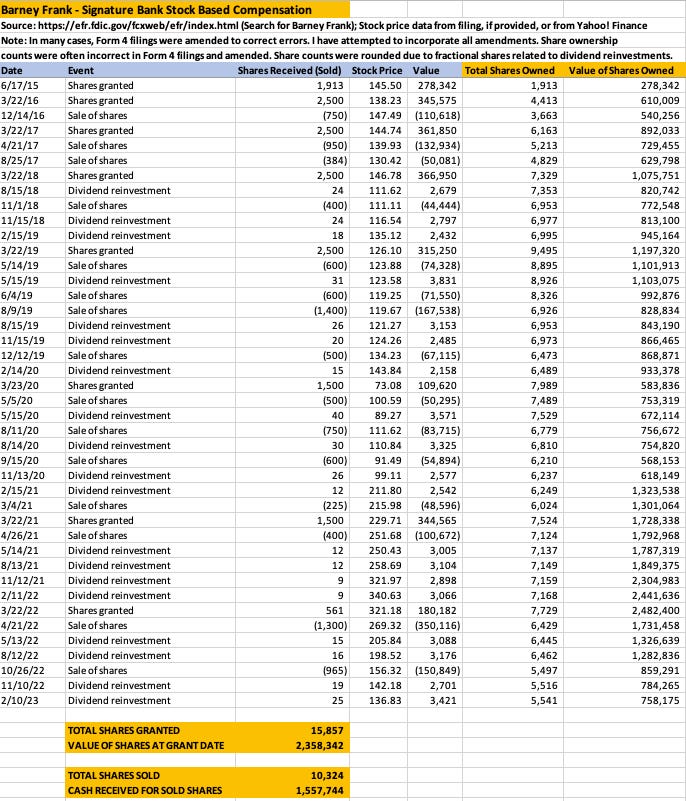

Mr. Frank’s name started to appear in articles today, including in this morning’s Wall Street Journal coverage of the Signature Bank failure. However, it seems like the mainstream media is still missing the real story when we are told that shareholders of these banks will likely be wiped out. It is probably true that the 5,541 shares of Signature Bank that Mr. Frank held at the date of his latest financial disclosure will end up being worthless, but my research indicates that he has received nearly $2 million in cash for serving on the bank’s board over the past eight years.

It is not difficult to dig up information on director compensation. For all the shortcomings of our financial system, at least directors, executives, and other insiders are required to file financial disclosures when they acquire and sell shares. In addition, proxy statements are required to disclose compensation. However, it takes a bit of work to look through dozens of filings to get the story.

Based on Signature Bank’s proxy statements for 2016 to 2023, Mr. Frank received the following cash compensation:

Personally, I think that five figure annual compensation for a (very) part time gig represents generous compensation, although it is far from the level that is routinely paid at many corporations. It appears that the bank was starting to reward directors more generously in 2022. After all, the cost of living is going up quite rapidly.

But cash compensation is only a small part of the story. Directors like Barney Frank end up with significant stockholdings, not because they put their own hard-earned money on the line but because they are awarded with generous stock grants every year. Unlike most employee stock based compensation plans, director stock based compensation usually has a very short vesting period. In the case of Signature Bank, stock awards for directors vest in just one year.

The information on stock based compensation in proxy statements is of limited value when it comes to understanding how much cash directors ended up with over time. To better understand the actual cash received by Mr. Frank, I went through dozens of Form 4 filings which reveal the dates when stock was granted and sold over time. The following exhibit shows all of the stock grant and sale activity disclosed by Mr. Frank during his directorship of Signature Bank:

The disclosures reveal that Mr. Frank was granted a total of 15,857 shares worth $2.36 million on the date of the grants (including dividend reinvestments). Through a series of sales, Mr. Frank received cash of $1.56 million for 10,324 shares.

Why was Barney Frank selected for the Signature Bank board of directors? The company’s 2022 proxy statement provides a predictable answer:

“Barney Frank has been a member of the Board since June 2015. Mr. Frank served as a U.S. Congressman representing the 4th District of Massachusetts from 1981-2013 and also was the Chairman of the House Financial Services Committee from 2007-2011. As Chair of the House Financial Services Committee, Mr. Frank was instrumental in crafting the short-term $550 billion rescue plan in response to the nation’s 2008-2009 financial crisis. Later, he co-sponsored the Dodd-Frank Wall Street Reform and Consumer Protection Act, which was signed into law in July 2010. Prior to serving in Congress, Mr. Frank spent eight years as a state Representative in Massachusetts and, earlier, served as Chief of Staff to Congressman Michael Harrington and Chief Assistant to Mayor Kevin White of Boston. Mr. Frank’s extensive experience as a Congressman, and particularly as Chair of the House Financial Services Committee, led the Board to conclude that he should be a member of the Board.” [emphasis added]

Few would dispute Barney Frank’s familiarity with the banking system. Unfortunately, his accumulated experience from decades in government service apparently did not prevent Signature Bank from adopting a business strategy that resulted in failure.

Why was Barney Frank really on Signature Bank’s board?

I cannot read minds, but the presence of a former politician who was instrumental in creating the current framework of banking regulation was no doubt a feather in the cap of bank executives and was used as a prop to provide bank customers and financial markets with an aura of safety and credibility.

There is something grotesque about politicians retiring from “public service” and landing at corporations in the industries that they regulated and then extracting millions of dollars in compensation for what is, at best, a very part time job. Anyone with an ounce of common sense sees that this stinks to high heaven.

If current politicians and regulators see former politicians and regulators rewarded in this manner, they will get a clear message from the private sector: “Let’s be friends while you are in public service and we will take care of you once you retire.”

This is corrosive to the system and should be outright prohibited.

To be clear, there is no indication that Mr. Frank or the Signature Bank board of directors did anything illegal, and I am not alleging that they did. I am expressing the opinion that this entire arrangement was highly corrupt and utterly shameful. It’s unfortunate that we live in a society where shame is almost entirely absent.

Notes:

I obtained proxy statements from Signature Bank’s website.

I obtained Barney Frank’s Form 4 disclosures on the FDIC website by running a search on his name at https://efr.fdic.gov/fcxweb/efr/index.html. I was unable to find Mr. Frank’s disclosures on the SEC Edgar system.

If you found this article interesting, please click on the ❤️️ button and consider sharing this issue with your friends and colleagues. The Rational Walk no longer uses social media. Readers who use social media are encouraged to post links.

Thanks for reading!

Copyright and Disclaimer

Nothing in this article constitutes investment advice and all content is subject to the copyright and disclaimer policy of The Rational Walk LLC.

Your privacy is taken very seriously. No email addresses or any other subscriber information is ever sold or provided to third parties. If you choose to unsubscribe at any time, you will no longer receive any further communications of any kind.

The Rational Walk is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com.

Segments of a Barney Frank interview on his role at Signature Bank:

https://www.youtube.com/watch?v=cVHYG90F75Q

Segment on his compensation at Signature Bank, which I wrote about last week (starts at 3:20):

"I was looking for an ongoing source of income. So about 325K per year which I must say, it might sound a little arrogant, for an honors graduate of Harvard Law School, $325K per year is not an excessive salary."

How many hours per year did Barney "work" to "earn" that salary? As I documented in great detail, his CASH take from eight years on the Signature board was a bit under $2 million. Which I guess was a big sacrifice because that turns out to be around $250K/year, not $325K/year.

Barney Frank is the perfect example of corrupt, revolving door politics. This story has been lightly reported because Barney has the "correct" political views. I can only imagine the outrage if he was on the other side of the aisle (not that there aren't plenty of corrupt people on that side as well).

It was interesting to read a WSJ article today that stated that banks can be exempt from filing insider transactions with the SEC. This is why I could not find Barney Frank’s Form 4s on EDGAR and had to go digging through the FDIC database linked to above. Seems like a ridiculous rule — the filings should absolutely be on EDGAR where you can use RSS feeds for monitoring, as I do for dozens of companies. It was a real pain to have to use the FDIC database rather than EDGAR.

WSJ article: https://www.wsj.com/articles/first-republic-bank-executives-sold-12-million-in-stock-in-months-before-crash-ca6ce79e