A Very Strange Public Offering

The origin story of Berkshire Hathaway's Class B stock

“As I write this - with Berkshire stock at $36,000 - Charlie and I do not believe it undervalued. Therefore, the offering we propose will not diminish the per-share intrinsic value of our existing stock. Let me also put our thoughts about valuation more baldly: Berkshire is selling at a price at which Charlie and I would not consider buying it.”

— Warren Buffett, March 1,1996

Berkshire Hathaway is a very unconventional company. Every aspect of how Warren Buffett has structured Berkshire’s strategy and operations flies in the face of standard procedures taught in business schools. Berkshire’s approach would not be possible without shareholders who trust management and understand what they own. The seamless web of deserved trust that has developed over decades is no accident and can be illustrated by the strange origin story of Berkshire’s Class B common stock.

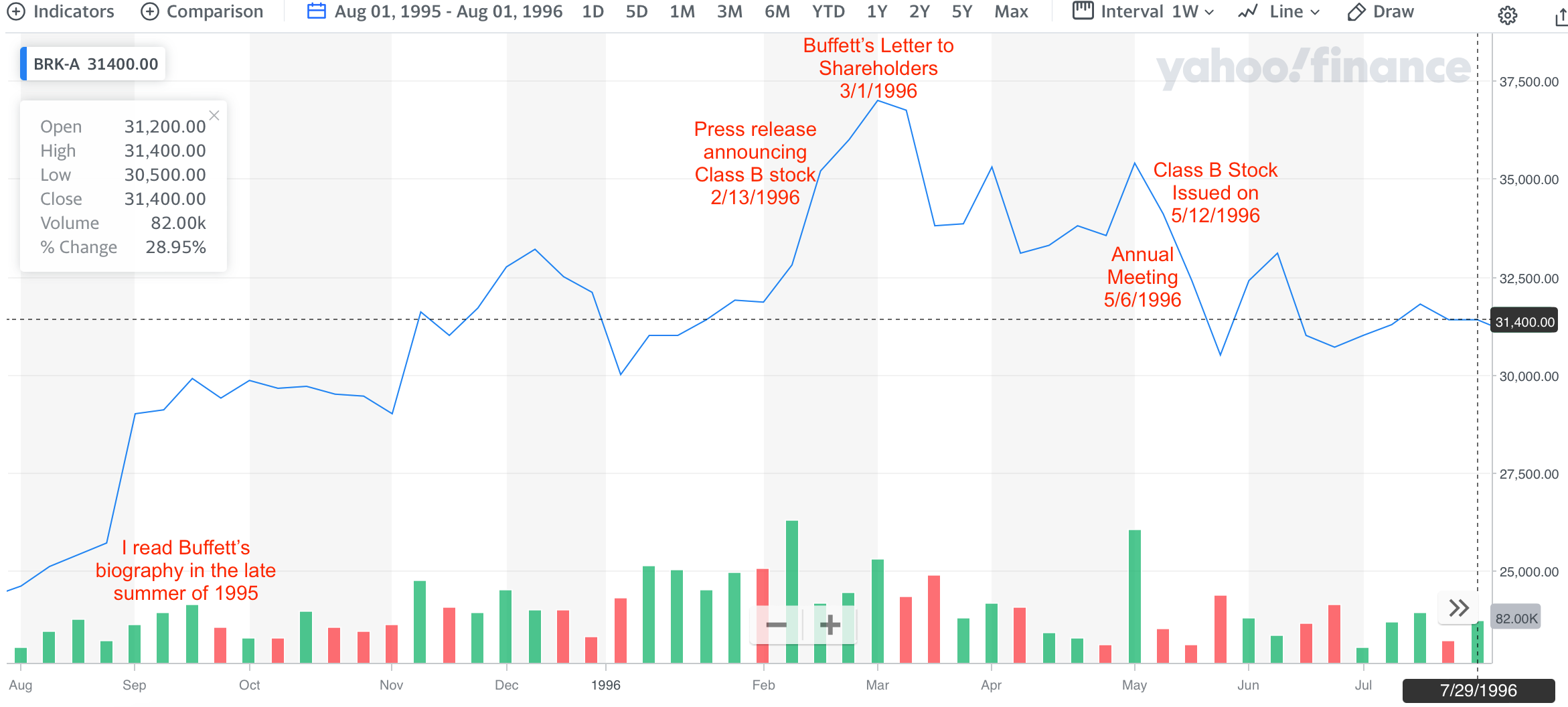

The history of the Class B stock offering is very much tied up with my own origin story as a Berkshire shareholder. I only became fully aware of Berkshire Hathaway’s remarkable history in the late summer of 1995 after reading Roger Lowenstein’s biography of Warren Buffett, The Making of an American Capitalist. I soon read Mr. Buffett’s shareholder letters and definitely wanted to own the stock.

As much as I wanted to buy shares, the stock traded around $25,000. I would have had trouble buying even one share as a new college graduate. Even putting aside the mantra of diversification that my finance professors had drilled into me for years, my entire net worth was about $20,000. Even if I was willing to put the sum of all of my savings from paper routes and various jobs into the stock, it would not be enough.

Over the next several months, I watched in dismay as the price of Berkshire’s stock rose steadily, closing the year above $32,000. By the time Warren Buffett’s 1995 shareholder letter appeared on March 1, 1996, the shares were trading at $36,000! Perhaps I would never be able to become a shareholder.

The following chart shows Berkshire’s stock price from August 1995 to July 1996 along with some of the key dates relevant to this story:

I was hardly alone in my frustration as a very small investor. Roger Lowenstein’s book raised Warren Buffett’s already high profile and most likely contributed to the rally in Berkshire’s stock in the months following the book’s publication. Although I was not aware of the development, promoters of “unit trusts” were poised to capitalize on the desire of small investors to invest in Berkshire, as Warren Buffett explained in his press release announcing the offering of Class B stock:

"Warren E. Buffett, Chairman of Berkshire Hathaway, explained the Company's proposed recapitalization as its reluctant response to certain largely-unpublicized moves that have been made by parties unaffiliated with Berkshire, eager to profit from the fact that Berkshire has chosen not to split its stock. These parties, in registration statements filed with the Securities & Exchange Commission, have indicated their intention to create unit investment trusts that would sell for relatively small amounts -- say $1,000 -- and that would purport to be miniature Berkshires or that would otherwise make an effort to associate themselves with Berkshire's reputation.”

What was the incentive for the promoters of these unit trusts? Obviously, they were motivated by the fees that could be charged to small investors who could not afford a single share of Berkshire Hathaway stock. Most likely, they would have charged hefty annual fees and possibly sales loads in exchange for doing very little work other than buying shares of Berkshire Hathaway in response to investor inflows. The owners of unit trust shares would experience performance that lagged Berkshire’s performance.

Who was the target market for the unit trusts? People in my boat who had read about Berkshire Hathaway and Warren Buffett and could not afford a single share!

The possibility of small investors being taken advantage of by unit trust promoters clearly infuriated Warren Buffett and Charlie Munger. Of course, the demand for unit trusts would evaporate if Berkshire would simply split its common stock. However, Mr. Buffett had long resisted requests to take such an action because he correctly viewed stock splits as doing absolutely nothing to change Berkshire’s underlying intrinsic value. In addition, a split could reduce the quality of the shareholder base by attracting buyers who think that stock splits have economic benefits.

In his letter to shareholders, Warren Buffett emphasized that he had nothing against small investors becoming owners but was worried that investors in the unit trusts would have unrealistic expectations and that Berkshire’s underlying performance was unlikely to meet those expectations, even aside from the unit trust fee structure:

"I did not discourage these people because I prefer large investors over small. Were it possible, Charlie and I would love to turn $1,000 into $3,000 for multitudes of people who would find that gain an important answer to their immediate problems.

In order to quickly triple small stakes, however, we would have to just as quickly turn our present market capitalization of $43 billion into $129 billion (roughly the market cap of General Electric, America's most highly valued company). We can't come close to doing that. The very best we hope for is - on average - to double Berkshire's per-share intrinsic value every five years, and we may well fall far short of that goal.”

The unit trusts would provide no value to its owners other than being “clones” of Berkshire — and inferior clones due to the drag of the commissions and fees. The primary motivation for the offering of Class B stock was to “make the clones unmerchandisable.” If small investors were going to own Berkshire, they would do so on terms that Warren Buffett approved of and with ample warning that he did not consider the company to be undervalued.

When was the last time that you heard of a company issuing stock with a warning that the valuation was too high?

How would the Class B shares make the unit trusts unmerchandisable?

As Mr. Buffett explained, the Class B stock would have economic rights equivalent to 1/30th of a Class A share and could be expected to trade at about 1/30th of the Class A. With the Class A shares trading around $36,000, we could expect the Class B shares to trade at around $1,200. (Note: The Class B stock split 50-for-1 in 2010.)

Although the economic rights of Class B stock were 1/30th of the Class A stock, Class B shares would have 1/200th of the voting power of Class A stock. In addition, each Class A share would be convertible to 30 Class B shares with no tax consequences, but Class B shares could not be converted to Class A. Finally, only Class A shareholders would be able to participate in a shareholder-designated charitable contributions program.

While the Class B stock would be inferior to Class A due to reduced voting rights and one-way convertibility, it would effectively provide a way for small investors to own an economic interest in the company without incurring the fees of unit trusts.

When I read about the upcoming Class B stock offering, I had mixed emotions.

It was not lost of me that I was the target market of the unit trusts. I did not know about the unit trusts but, had I been aware of them, I would have at least thought about making an investment. I’d like to think that I would have been cognizant of the effect of fees, but despite having a finance background, I might have still invested.

I was very eager to participate in the Class B offering but Warren Buffett’s statement on Berkshire Hathaway not being undervalued bothered me. I was less familiar with Mr. Buffett then than I am now so the thought occurred to me that his warning was a necessity due to securities regulations. Maybe he had to issue these warnings.

This thought evaporated when I read this all-caps statement in the offering document:

WARREN BUFFETT, AS BERKSHIRE'S CHAIRMAN, AND CHARLES MUNGER, AS BERKSHIRE'S VICE CHAIRMAN, WANT YOU TO KNOW THE FOLLOWING (AND URGE YOU TO IGNORE ANYONE TELLING YOU THAT THESE STATEMENTS ARE "BOILERPLATE" OR UNIMPORTANT):

1. Mr. Buffett and Mr. Munger believe that Berkshire's Class A Common Stock is not undervalued at the market price stated above. Neither Mr. Buffett nor Mr. Munger would currently buy Berkshire shares at that price, nor would they recommend that their families or friends do so.

2. Berkshire's historical rate of growth in per-share book value is NOT indicative of possible future growth. Because of the large size of Berkshire's capital base (approximately $17 billion at December 31, 1995), Berkshire's book value per share cannot increase in the future at a rate even close to its past rate.

3. In recent years the market price of Berkshire shares has increased at a rate exceeding the growth in per-share intrinsic value. Market overperformance of that kind cannot persist indefinitely. Inevitably, there will also occur periods of underperformance, perhaps substantial in degree.

4. Berkshire has attempted to assess the current demand for Class B shares and has tailored the size of this offering to fully satisfy that demand. Therefore, buyers hoping to capture quick profits are almost certain to be disappointed. Shares should be purchased only by investors who expect to remain holders for many years.

In order to issue Class B stock, Berkshire Hathaway had to get shareholder approval at the annual meeting on May 6, 1996. At the meeting, Mr. Buffett expanded on his rationale for creating the Class B stock. The video below is one of several clips available on the CNBC Warren Buffett Archive pertaining to the Class B offering:

In statements during the annual meeting as well as in his letter to shareholders, Mr. Buffett was doing all he could to discourage investors from purchasing Class B stock.

Did he really mean what he was saying?

I faced the following options:

I could disregard Mr. Buffett’s statements and assume he did not really believe what he kept saying again and again. I could buy the stock. However, if I did so, I would be taking the risk that he really did mean what he was saying and I could overpay for the stock. Also, it occurred to me that if Mr. Buffett did not really believe what he was saying, that would call into question my impression of how Berkshire was run and my desire to be an owner of the company.

I could take Mr. Buffett’s statements at face value and refrain from making any purchase since he did not consider the stock undervalued and, more importantly, would not even recommend it to his friends or family! I would not be a Berkshire shareholder but could still follow the company, learn more about the business, and try to understand the stock’s valuation for myself. At this point, I had no independent view of Berkshire’s value other than Mr. Buffett’s statements.

Upon further reflection, I decided that I had no choice but to take the second option. It would make no sense to become a shareholder at a price that Warren Buffett himself considered too expensive. Indeed, doing so would be ridiculous for someone who, at that time, wanted to emulate Mr. Buffett by picking undervalued stocks! I decided to watch the company and hope for a better entry point.

The mechanics of the offering of Class B shares in May 1996 were designed to avoid a speculative bubble in the stock. When Berkshire announced plans to issue the stock in February 1996, the company committed to issuing at least $100 million of Class B shares. However, because Warren Buffett did not consider the stock undervalued, he was willing to increase the size of the offering as much as needed to meet initial demand. In Berkshire’s 10-Q for the second quarter of 1996, the company announced that 517,500 shares were issued resulting in net proceeds to Berkshire of $565 million. The offering had to be increased by more than five times to satisfy initial demand.

The combination of Mr. Buffett’s warnings about Berkshire’s valuation and his willingness to issue as many Class B shares as needed to satisfy demand succeeded in preventing a bubble in the stock. In fact, Berkshire’s Class A and Class B stock treaded water for the rest of 1996 before taking off like a rocket in 1997 and 1998.

For my part, I recall being tempted to buy shares later in 1996 but I never did. I watched the stock rise over the next few years as well as its subsequent decline as the dot com bubble inflated and Berkshire was seen as a stodgy “old economy” dinosaur. Troubles related to the General Re acquisition in 1998 also contributed to a steep decline in the stock as the turn of the century approached:

The truth is that I was not ready to purchase the stock in 1996 regardless of the availability of the Class B shares or the valuation of the company. I had no real understanding of Berkshire at that time aside from reading Warren Buffett’s biography and the shareholder letters. But I kept following the company and purchased my first shares on February 15, 2000. I somehow added shares on March 9, 2000 which turned out to be Berkshire’s low and I added more shares on March 28, 2000.

Since this story might seem like I’m bragging, or at least “humble bragging”, I assure the reader that it involved much more luck than skill.

I knew more about Berkshire in early 2000 than I did in 1996 but I do not recall having an independent view of intrinsic value, nor did I keep an investing journal or any other records at the time that would reveal my buy rationale. However, I do still own those shares of Berkshire and suppose I deserve some credit for holding for nearly a quarter century. I also kept learning more and more about Berkshire and eventually started writing about the company, first privately in the mid 2000s and later in public when I started The Rational Walk in early 2009 which was another dark time for Berkshire Hathaway’s stock. By then, I was well equipped to hold through tough times.

If you find this article interesting, please click on the ❤️️ button and consider sharing it with your friends and colleagues.

Thanks for reading!

The story of Berkshire’s Class B stock would be incomplete without revisiting Warren Buffett’s warnings back in the spring of 1996. Were his warnings justified?

The crux of the matter is not really Berkshire’s valuation in early 1996. I suspect the much larger problem troubling Mr. Buffett at the time involved unrealistic expectations about how fast he could compound Berkshire’s intrinsic value going forward. I’ll repeat a portion of the quote from his 1995 annual letter presented earlier:

“In order to quickly triple small stakes, however, we would have to just as quickly turn our present market capitalization of $43 billion into $129 billion (roughly the market cap of General Electric, America's most highly valued company). We can't come close to doing that. The very best we hope for is - on average - to double Berkshire's per-share intrinsic value every five years, and we may well fall far short of that goal.”

If Warren Buffett thought that he could continue compounding capital at over 20%, as he had for three decades, would it have mattered if new shareholders slightly overpaid for Class B shares? It is difficult to overpay for a company that can triple intrinsic value in a few years. This is why Mr. Buffett stated that he could not come close to delivering such results. The very best he hoped for was doubling intrinsic value every five years which is the equivalent of delivering a 15% compound annual return.

In reality, Berkshire has not been able to compound at anywhere near 15% since the Class B shares were offered to investors.

According to Yahoo! Finance, Class B shares closed at $1,200 on May 10, 1996. Note that this is the equivalent of $24 on a split adjusted basis accounting for the 50-for-1 split of the Class B stock in 2010. With the stock trading around $358 on August 11, 2023, the shares delivered a 10.43% compound annual return over 27 1/4 years.

If Berkshire had been able to compound at 15% over the past 27 1/4 years, the Class B shares would trade around $1,082!

So it was justified for Warren Buffett to warn investors to not expect him to match the exceptional returns that he delivered from 1965 to 1996 starting from a tiny base of capital. It would have been unrealistic to believe that he could pull off such a feat. However, even buying at a price that Mr. Buffett considered overvalued, those who purchased Class B shares at the offering and held up to today would have earned a very satisfactory return given that the S&P 500 has only compounded at ~9.2% over the same approximate period (May 1996 to July 2023) assuming reinvestment of dividends.

For my part, I am glad that I waited until 2000 to buy shares, not only because my compound annual return is meaningfully better than if I had purchased at the initial offering, but because I probably would have sold the stock sometime in 1997 or 1998 and perhaps I would not have repurchased the stock in subsequent years. The truth is that I was poorly equipped to own Berkshire or any other stock at that time in my life. I credit Warren Buffett’s warning for the fact that I waited to buy until I had a better long term owner’s mindset and was equipped to hold for the long run.

Copyright, Disclosures, and Privacy Information

Nothing in this article constitutes investment advice and all content is subject to the copyright and disclaimer policy of The Rational Walk LLC.

Your privacy is taken very seriously. No email addresses or any other subscriber information is ever sold or provided to third parties. If you choose to unsubscribe at any time, you will no longer receive any further communications of any kind.

The Rational Walk is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com.

Long Berkshire Hathaway.

Stories of seeing interesting companies people own shares of for decades are hard to come by and always carry insight!

I am up to 2003 listening to the Berkshire Annual Meeting archives. Anybody can also hear it from the horses’ mouths recorded in real time. In the years before brk.b shareholders are bringing it up in the Q&A.