A Tale of Three Acquisitions

XTRA, Alleghany, and Twitter

“The right culture, the highest and best culture, is a seamless web of deserved trust. Not much procedure, just totally reliable people correctly trusting one another.”

Without a certain level of trust, our modern civilization would soon disintegrate into total chaos. Like oxygen, many of us tend to take trust for granted until it is in short supply. Trust is particularly important in business. You might be given the benefit of the doubt initially, but abuse of that trust is likely to ruin your reputation and severely curtail future opportunities. This is true on Main Street, and it is true on Wall Street.

Let’s take a brief look at the role of trust in three acquisitions.

XTRA Lease Company

In June 2001, Julian Robertson called Warren Buffett to let him know that he had decided to sell his 27% ownership interest in XTRA, a leading lessor of truck trailers. This prompted Mr. Buffett to initiate talks with XTRA’s CEO regarding the possibility of acquiring the company. On July 31, 2001, Berkshire and XTRA announced a merger agreement for $590 million. The acquisition was to be effectuated through a tender offer expiring on … September 11, 2001.

As Mr. Buffett described in his 2001 letter to shareholders, Berkshire had the ability to get out of the deal if the stock market were to close prior to the expiration of the tender offer. The terrorist attacks of September 11, 2001 did cause a market closure and Berkshire could have exited the deal. However, Mr. Buffett chose to proceed despite the fact that the attacks were sure to result in large insurance losses for Berkshire. Additionally, XTRA is a cyclical business, and its valuation would likely have dropped significantly once the markets reopened.

Why would Warren Buffett proceed with a $590 million deal that could have probably been renegotiated or abandoned entirely? The answer is straight-forward: When Berkshire Hathaway makes a deal to acquire a company, it needs to be as good as cash in the bank. This has been a competitive advantage for Berkshire over many decades and there was no way Mr. Buffett was going to risk losing that reputation. Berkshire closed on the deal for the agreed upon price.

Alleghany Corporation

On March 21, 2022, Berkshire Hathaway agreed to acquire Alleghany Corporation in an all-cash deal for $848.02 per share which I discussed at length on the day the deal was announced. Warren Buffett agreed to give Alleghany a 25-day “go shop” period to solicit superior bids, but none were forthcoming. The deal is expected to close in the fourth quarter of 2022, and the market believes that it certainly will close as scheduled. How do we know what the market believes? Take a look at the Alleghany stock chart:

We can see that the stock price shot up on the day of the announcement and even slightly exceeded the $848.02 offer price. Why would the stock have exceeded the offer price? During the 25-day “go shop” period, market participants were willing to pay a premium for the possibility of a higher bid emerging. When it became clear that this would not occur, the stock fell below the $848.02 offer, and it currently trades at around $836.

The chart shows that the stock has traded with very little variation over the past few months indicating that the market expects the deal to go through. The ~1.5% discount to the deal price simply reflects the time value of money between now and when the market expects the deal to close in the fourth quarter combined with perhaps a very small risk premium.

How has the broader insurance industry performed in the stock market since the deal was announced? The SPDR S&P Insurance ETF ($KIE) tracks the S&P Insurance Industry Index. The ETF closed at $41.06 on March 21 and is trading at $37.29 as I type this in the mid-afternoon on July 22. This is a decline of 9.2% since Berkshire’s deal for Alleghany was announced. Berkshire Hathaway’s stock is down 18.6% over the same period. If Berkshire had not made an offer for Alleghany, it is nearly certain that Alleghany stock would be trading far lower than it is today.

Despite the decline in stock prices, market participants do not believe that Warren Buffett will try to find some technicality to exit the deal for Alleghany. The reason the market is so confident is because of Mr. Buffett’s track record. Everyone trusts that when someone makes a deal with Berkshire, that deal is as good as cash in the bank.

Twitter

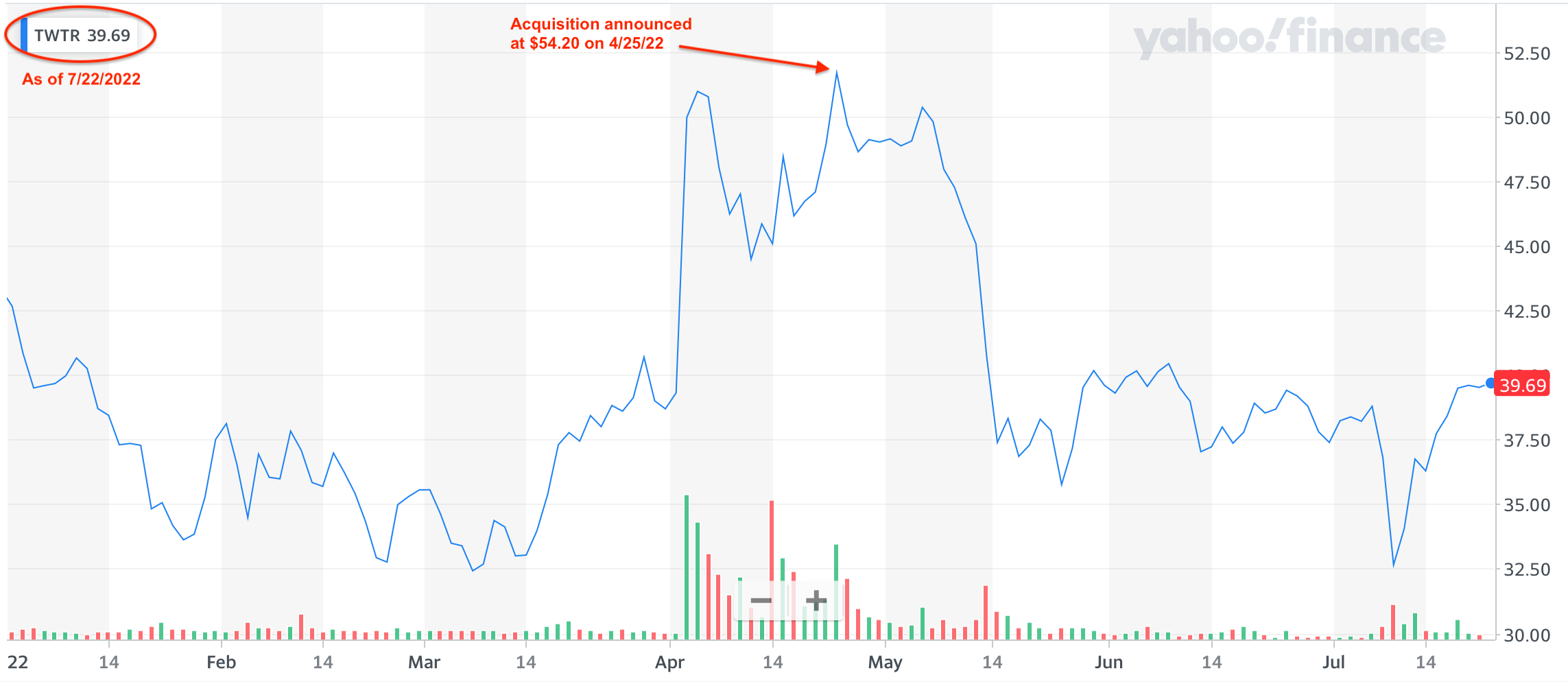

On April 4, Elon Musk filed a disclosure revealing that he had purchased a 9.2% stake in Twitter. Based on that purchase and Mr. Musk’s many tweets regarding the company, Twitter stock shot up in anticipation that he would make an offer for the entire company. On April 14, Mr. Musk offered $54.20 per share to acquire the company. On April 25, Twitter agreed to be acquired by Mr. Musk for $54.20 per share.

My point in bringing up Elon Musk’s offer for Twitter is that it serves as a stark contrast to Warren Buffett’s acquisitions when it comes to what market participants actually believe. If an offer from Berkshire Hathaway is as good as gold, how good is an offer from Mr. Musk?

The chart below shows Twitter’s stock price this year and the arrow indicates the date when Twitter and Elon Musk agreed to the deal at $54.20 per share. The stock spiked but never quite reached the deal price, and then it plummeted as Mr. Musk tweeted about the acquisition over the next several weeks. On July 8, Mr. Musk notified Twitter that he plans to terminate the deal.

During the weeks between the deal’s announcement and Mr. Musk’s termination letter, the market never really believed that the deal would go through. The stock traded at a deep discount to the $54.20 acquisition price, implying the opportunity to gain 40-50% if the deal went through. But few believed that the deal would go through because there was little trust in Elon Musk’s intentions.

Mr. Musk accuses Twitter of numerous material breaches of the agreement, with the most important alleged breach relating to fake user accounts. Twitter has sued Mr. Musk to force the merger to be completed on the terms agreed to on April 25.

Since April 25, the NASDAQ Composite index has declined by 9.2% and Meta Platform’s stock has declined by 9.6%. Twitter’s stock price, absent a bid from Elon Musk, would likely have fallen along with technology stocks. Many observers suspect that Mr. Musk simply got cold feet once he saw the overall decline in technology stocks as well as the decline in Tesla’s stock in the weeks after the merger agreement.

If I attempted to chronicle the many twists and turns that this saga has taken over the past three months, this short article would become a 5,000 work treatise and there are plenty of better sources for that story. I highly recommend Matt Levine’s reporting on the subject which has left few stones unturned.

Let’s Make a Deal …

Obviously, Warren Buffett and Elon Musk are not likely to be in direct competition for acquisitions, but that isn’t the point of the comparison. Elon Musk will be in a position where he must negotiate deals in the future, and not just for acquisitions. Credibility and trust are paramount when it comes to deals and it seems like Mr. Musk has lost a great deal of credibility due to his Twitter bid. This could come back to haunt him in the future.

When it comes to acquisitions, the trust and certainty of making a deal with Berkshire adds up to real savings for the company. There are many instances where a seller would take a slightly lower offer from Berkshire knowing that it will absolutely close as scheduled rather than taking a somewhat higher offer from a less certain bidder.

A deal with Warren Buffett is a deal you can take to the bank. Barring some egregious instance of outright fraud or intentional deception, he is not going to try to back out of an agreement, and not just for acquisitions. Berkshire enters into all sorts of other transactions in which trust is critical, with insurance being an obvious example. How much money has Berkshire made over the years by operating in the spirit of Charlie Munger’s seamless web of deserved trust?

Elon Musk might have many positive attributes but without trust, he will face many more hurdles accomplishing his future aspirations. Traveling to Mars and colonizing the planet is going to be impossible without the cooperation of numerous private and public entities and it will all require a great deal of trust to accomplish.

For more on the advantage of trust at Berkshire Hathaway, I recommend The Berkshire Handshake by Kingswell published on July 14, 2022. The article discusses the role of trust in Berkshire’s acquisition of Nebraska Furniture Mart in 1983.

The Rational Walk is a reader-supported publication

To support my work and to receive all articles that I publish, including premium content, please consider a paid subscription. Thanks for reading!

Copyright, Disclosures, and Privacy Information

Nothing in this newsletter constitutes investment advice and all content is subject to the copyright and disclaimer policy of The Rational Walk LLC.

Your privacy is taken very seriously. No email addresses or any other subscriber information is ever sold or provided to third parties. If you choose to unsubscribe at any time, you will no longer receive any further communications of any kind.

The Rational Walk is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com.

I would not own stock in a company owned or controlled by Musk. Life is too short. In contrast, Berkshire Hathaway is my largest holding.

Nice, concise, fun read